DynaResource Reports Year End 2025 Results at the San Jose de Gracia Mine, Net Income for 2025 of $3.8M, and Adjusted EBITDA for 2025 of $12.1M

All figures in United States Dollars (“USD”).

Irving, Texas–(Newsfile Corp. – April 1, 2026) – DynaResource, Inc. (OTCQX: DYNR) (“DynaResource”, or the “Company”) is pleased to report results for the fourth quarter and fiscal year ended December 31, 2025 at the San Jose de Gracia mine (the “SJG mine”) highlighted by continued financial momentum with both gross profit and adjusted EBITDA demonstrating continued growth.

Full Year and Q4 2025 Highlights:

-

Revenue increased 26% to $58.5 million in 2025 from $46.5 million in 2024 while Q4 2025 revenue of $14.8 million was up from $14.1 million in the previous quarter.

-

Full year 2025 net income of $3.8 million, compared to net loss of $8.5 million in 2024. Q4 2025 net income of $1.4 million compared to net loss of $0.3 million in Q4 2024 and $1.3 million in Q3 2025.

-

Adjusted EBITDA for the 12 months ending 2025 was $12.1 million compared to negative $1.3 million for the twelve months ending 2024. Q4 2025 demonstrated the fifth consecutive quarter of positive adjusted EBITDA totaling $4.7 million compared to $1.4 million in Q4 2024 and $1.4 million in Q3 2025.

-

Full year 2025 gold production of 21,393 ounces fell within the Company’s revised guidance. Q4 2025 gold production of 5,080 ounces compared to 4,830 ounces in Q3 2025 and 6,775 ounces in Q4 2024.

-

Milled throughput in 2025 was 262,224 tons representing an increase of 257,676 tons over 2024. Milled throughput of 65,275 tons versus 62,741 tons in Q3 2025 and 67,670 tons in Q4 2024.

-

Daily mill throughput average of 718 tons per day in 2025, an increase over 2024.

Rohan Hazelton, President & CEO DynaResource stated, “We delivered solid operational results in 2025, underscoring the strength of our San Jose de Gracia mine and the team’s continued focus on disciplined execution. This translated into strong financial momentum in the fourth quarter and across the full year, with revenues, net income, and adjusted EBITDA demonstrating meaningful growth. These results reflect improved efficiencies at both the operating and corporate levels, alongside a continued emphasis on cost management as well as higher gold prices. With the sustained improvements in net income and adjusted EBITDA, the Company hopes to see its valuation increasingly reflect the underlying quality of the mine and performance of its operations.”

Quarterly Results for the Three and Twelve Months Ended December 31, 2025 and 2024:

| Three Months Ended | Twelve Months Ended | ||||||||||||

| Key Operating Information | Unit | December 31, 2025 | December 31, 2024 | December 31, 2025 | December 31, 2024 | ||||||||

| Operating Data | |||||||||||||

| Ore mined | t | 74,984 | 59,490 | 287,878 | 233,782 | ||||||||

| Mining rate | tpd | 815 | 647 | 789 | 639 | ||||||||

| Ore Milled | t | 65,275 | 67,670 | 262,224 | 257,676 | ||||||||

| Mill Throughput | tpd | 710 | 736 | 718 | 704 | ||||||||

| Grade | g/t | 3.20 | 4.12 | 3.46 | 4.07 | ||||||||

| Recovery Au | % | 75.68% | 75.58% | 73.69% | 76.24% | ||||||||

| Gold Ounces Produced | oz | 5,080 | 6,775 | 21,393 | 25,677 | ||||||||

| Gold Ounces Sold | oz | 4,767 | 6,897 | 20,848 | 22,003 | ||||||||

(1) Gold concentrate sold during the period is not equal to gold concentrate recovered during the period due to timing of shipments to buyer, and due to buyer’s payability discount for the purchase of gold concentrate, and due to any adjustment from dry weight and assay in provisional settlements with the final assays.

| Three Months Ended | Twelve Months Ended | ||||||||||||

| Corporate Financial Highlights | Unit | December 31, 2025 | December 31, 2024 | December 31, 2025 | December 31, 2024 | ||||||||

| Key Financial Data | |||||||||||||

| Total revenue | $ | 14,765,289 | 14,787,053 | 58,467,565 | 46,503,016 | ||||||||

| Total operating expenses | $ | 1,487,986 | 8,584,248 | 41,187,570 | 47,898,208 | ||||||||

| Gross Profit | $ | 13,277,303 | 6,202,805 | 17,279,995 | (1,395,192 | ) | |||||||

| Net income (loss) | $ | 1,452,485 | 71,445 | 3,817,103 | (8,521,443 | ) | |||||||

| Operating cash flows before change in non-cash working capital items | $ | (3,089,893 | ) | 738,946 | 3,634,203 | (7,445,914 | ) | ||||||

| Changes in working capital | $ | 4,885,941 | 260,523 | 2,122,945 | (568,090 | ) | |||||||

| Cash flow used in operating activities | $ | 1,796,048 | 999,469 | 5,757,148 | (8,014,004 | ) | |||||||

Summary of Site-Based Processing and Operational Activity, 2018 to 2025

| Year | Total Tons Processed |

Reported Mill Feed Grade (g/t Au) |

Reported Recovery % |

Gross Gold Concentrates Produced (Au oz.) |

Net Gold (1) Concentrates Sold (Au oz.) |

|||||

| 2018 | 52,038 | 9.82 | 86.11 | % | 14,147 | 13,418 | ||||

| 2019 | 66,031 | 5.81 | 86.86 | % | 10,646 | 9,713 | ||||

| 2020 | 44,218 | 5.65 | 87.31 | % | 7,001 | 5,828 | ||||

| 2021 | 97,088 | 9.67 | 88.79 | % | 26,728 | 22,566 | ||||

| 2022 | 137,740 | 8.18 | 88.05 | % | 31,905 | 25,554 | ||||

| 2023 | 198,518 | 5.58 | 76.50 | % | 27,252 | 24,829 | ||||

| 2024 | 257,676 | 4.07 | 76.24 | % | 25,677 | 22,003 | ||||

| 2025 | 260,694 | 3.46 | 73.69 | % | 21,393 | 20,848 |

Operational Performance Overview

During Q4 2025, the Company continued to advance the optimization program at the SJG mine. This program is focused on increasing process plant throughput and recoveries, improving maintenance and equipment utilization, and ultimately enhancing operational efficiencies and profit margins at the SJG mine.

Operational results for Q4 2025 showed improved performance across several critical operational metrics (particularly in costs) due to the ongoing optimization program. The average underground development was 1,057 meters per month in Q4 2025 (1,267 in Q3 2025), compared to 383 meters per month in Q4 2024. This increase allowed the SJG mine to access over 20 production stopes. Expanded development work also led to the discovery of two new mineralized veins – one at the Tres Amigos mine (named Victoria) and one at La Mochomera (named 532) which are currently being mined as additional high-grade ore sources. Process plant reliability also improved. Electrical refurbishment and preventative maintenance programs resulted in ball mill availability averaging 96% for Q4 2025 compared to 94% Q3 2025.

A construction work program to establish a primary gravity gold circuit with the installation of three new Falcon gravity concentrators (the “Falcon” units) was completed in Q3 2025 with commissioning completed in early Q4 2025. These Falcon units were installed after the ball mills to recover the significant portion of free gold available in the San Pablo, San Pablo Sur and La Mochomera deposits. In addition, the process plant at the SJG mine has another Falcon unit already installed on the tailings circuit. The aim of the installation of these Falcon units is to boost gold recoveries improving operational efficiency and SJG mine’s economics, especially in the current higher priced gold environment.

Milled ore for Q4 2025 was 65,275 tons (approximately 710 tons per day), a 4% increase from the Q3 2025 production average of 682 tons per day. With the current high ball mill availability, the Company is evaluating cost-effective strategies to utilize additional processing capacity of approximately 100 tons per day. Gold metal recoveries for the quarter averaged 75.69%, an increase from the 73% gold recovery achieved in Q3 2025, primarily due to the installation and commissioning of the Falcon units.

During Q4 2025, metal production totaled 1,633 ounces of gold in October, 1,615 ounces in November, and 1,832 ounces in December. Total metal production for Q4 2025 was 5,080 ounces of gold, above Q3 2025 production of 4,830 ounces. The average gold feed grade was 3.20 g/t for Q4 2025, and for the full year 2025, the average gold feed grade was 3.46 g/t.

Mine development for Q4 2025 was on budget with 3,172 meters of development completed, compared to 3,013 meters in Q3 2025. The completion of new development drifts enabled the Company to maintain more than 20 stopes in production by the end of the quarter and the end of the year. This additional mining flexibility is expected to positively impact ore tonnage and grades in the coming months in 2026. The Company has also completed a capital works program to enhance mine ventilation across all three mines which included connecting the La Mochomera and San Pablo Sur mines which has had an immediate impact on the working environment. Improved ventilation time has resulted in an improvement in working conditions and faster re-entry times following blasting activities. Planning for a central Raise Bore ventilation shaft was cancelled due to unfavorable geotechnical conditions and this planned ventilation location was moved to Palos Chinos. This capital works program will involve approximately 100 meters of decline development which, in addition to helping ventilation will bring mine development closer to the Purisima historical works. Numerous exploration targets have been identified in this southern area of the mineral field. This ventilation development will also be a platform for underground exploration.

Detailed activities from the four main deposits include:

Tres Amigos

Original mine planning at Tres Amigos anticipated closure by the end of Q1 2025. However, geological reinterpretations and targeted short exploration drifts identified two additional mineralized structures – the Victoria and Alexa veins – located within 40 meters of existing underground infrastructure.

To date approximately 40,000 tons of high-grade ore have been extracted from this high-grade structure. In addition, a new ore drive was completed on the upper levels of the Tres Amigos North Zone which is an area well known for free gold occurrences, providing access to a new high-grade ore face. Mining from this area in Tres Amigos totaled 17,000 tons contributing to Q4 2025 production and is expected to continue throughout 2026. This new access will also enable future diamond drilling to test the north and south extensions of the deposit, with the goal of increasing inventory.

San Pablo Viejo and San Pablo Sur

Throughout Q4 2025, the Company continued mining multiple faces at the San Pablo deposit while advancing development toward the deeper southern extensions.

San Pablo Viejo and San Pablo Sur are expected to remain the primary sources of gold production through 2026 and 2027, with additional upside potential beyond that horizon. Particularly promising is the South Extension at the 500 level, which could yield high-grade (“Bonanza”-style) gold mineralization in the short to mid-term. Ongoing development efforts are positioning the mine for continued growth, including expansion deeper into the La Mochomera vein system.

La Mochomera

The La Mochomera vein is expected to be a significant source of gold production in 2026 and 2027, with especially promising high-grade potential at depth. During Q1 2025, development activities intersected a previously unrecognized high-grade mineralized structure, now designated as the “532 Vein”. The significance and potential of this new discovery are currently being evaluated with approximately 3,000 tons of high-grade material extracted from this vein.

Palos Chinos

Palos Chinos is an ore body which the Company exposed in January 2025 from the La Mochomera underground infrastructure with the first ore being extracted in January 2025. By the end of Q4 2025, the Company had completed 4 development levels on this vein and mined 3,500 tons of ore. In 2026, this ore body will be an important source of high-grade ore.

Outlook at San Jose de Gracia

With the development progress achieved in Q4 2025 and the increase in mining faces now available to the Company, management remains confident in the ongoing progress and long-term performance of the SJG mine. The Company’s focus for 2026 is to improve production and grade through the implementation of additional and ongoing operational enhancements and development work.

While the Company made significant headway in 2025, optimization efforts will continue to focus on improving gold ore grades to the mill, throughput rates, and recoveries. San Pablo Sur, San Pablo, La Mochomera, Palos Chinos and the Tres Amigos ore bodies are expected to remain the main contributors to production in the year ahead. Further development in these areas will also be a key focus to access additional high-grade zones and additional mining faces.

The capital works program to add a primary gravity gold circuit to the processing plant involved the installation of three new Falcon units installed downstream of the ball mills to recover the significant portion of the free gold present in the San Pablo, San Pablo Sur, Tres Amigos and La Mochomera deposits. The three new Falcon units are performing as designed recovering approximately 30% of the gold in a specific gravity gold concentrate (average ~300 g/t Au) which achieves a higher payability factor. The target for 2026 is for the process plant to achieve a processing rate between 750 to 800 tpd.

A new tailings dam was completed during Q3 2024, with an estimated storage capacity of 670,751 cubic meters, distributed over four stages to accommodate up to three years of additional tailings. The third-stage facility is currently in use, and planning for construction of the fourth stage is underway. The Company has also begun evaluating a potential location for a third tailings storage facility at the SJG mine. These studies include environmental and geotechnical surveys to identify a preferred site.

On behalf of the Board of Directors of DynaResource, Inc.

Rohan Hazelton

President & CEO

About DynaResource

DynaResource is a junior gold mining producer trading on the OTCQX under the symbol “DYNR”. DynaResource is actively mining and expanding the historic San Jose de Gracia gold mining district in Sinaloa, Mexico.

For Information on DynaResource, Inc. please visit www.dynaresource.com, or contact:

Investor Relations:

Katherine Pryde, Investor Relations Manager

+1 972-869-9400

info@dynaresource.com

CAUTIONARY NOTE REGARDING FORWARD-LOOKING INFORMATION

This news release contains forward-looking statements within the meaning of Section 27 A of the Securities Act of 1933 and Section 21E of the Securities Exchange Act of 1934.

Certain information contained in this news release, including any information relating to future financial or operating performance may be deemed “forward-looking”. All statements in this news release, other than statements of historical fact, that address events or developments that DynaResource expects to occur, are “forward-looking information”. These statements relate to future events or future performance and reflect the Company’s expectations regarding the future growth, results of operations, business prospects and opportunities of DynaResource. These forward-looking statements reflect the Company’s current internal projections, expectations or beliefs and are based on information currently available to DynaResource. In some cases, forward-looking information can be identified by terminology such as “may”, “will”, “should”, “expect”, “intend”, “plan”, “anticipate”, “believe”, “estimate”, “projects”, “potential”, “scheduled”, “forecast”, “budget” or the negative of those terms or other comparable terminology. Certain assumptions have been made regarding the Company’s plans at the San Jose de Gràcia property. Many of these assumptions are based on factors and events that are not within the control of DynaResource and there is no assurance they will prove to be correct. Such factors include, without limitation: capital requirements, fluctuations in the international currency markets and in the rates of exchange of the currencies of the United States and México; price volatility in the spot and forward markets for commodities; discrepancies between actual and estimated production, between actual and estimated reserves and resources and between actual and estimated metallurgical recoveries; changes in national and local governments in any country which DynaResource currently or may in the future carry on business; taxation; controls; regulations and political or economic developments in the countries in which DynaResource does or may carry on business; the speculative nature of mineral exploration and development, including the risks of obtaining necessary licenses and permits, diminishing quantities or grades of reserves; competition; loss of key employees; additional funding requirements; actual results of current exploration or reclamation activities; changes in project parameters as plans continue to be refined; accidents; labor disputes; defective title to mineral claims or property or contests over claims to mineral properties. In addition, there are risks and hazards associated with the business of mineral exploration, development and mining, including environmental hazards, industrial accidents, unusual or unexpected formations, pressures, cave-ins, flooding and gold bullion losses (and the risk of inadequate insurance or inability to obtain insurance, to cover these risks) as well as those risks referenced in the Annual Report on Form 10-K for DynaResource available at www.sec.gov. Forward-looking information is not a guarantee of future performance and actual results, and future events could differ materially from those discussed in the forward-looking information. All of the forward-looking information contained in this news release is qualified by these cautionary statements. Although DynaResource believes that the forward-looking information contained in this news release is based on reasonable assumptions, readers cannot be assured that actual results will be consistent with such statements. Accordingly, readers are cautioned against placing undue reliance on forward-looking information. DynaResource expressly disclaims any intention or obligation to update or revise any forward-looking information, whether as a result of new information, events or otherwise.

NON-GAAP FINANCIAL PERFORMANCE MEASURES

We have included adjusted EBITDA as a supplemental measure of our performance in this press release. In the gold mining industry, adjusted EBITDA is a common performance measure but does not have any standardized meaning and is considered a non-GAAP financial measure. We define adjusted EBITDA as net income (loss) plus (i) interest expense, (ii) provision for taxes, and (iii) depreciation and amortization, as further adjusted to eliminate the impact of certain items that we do not consider indicative of our ongoing operating performance. These further adjustments are itemized below. You are encouraged to evaluate these adjustments and the reasons we consider them appropriate for supplemental analysis. In evaluating adjusted EBITDA, you should be aware that in the future we may incur expenses that are the same as or similar to some of the adjustments in this presentation. Our presentation of adjusted EBITDA should not be construed as an inference that our future results will be unaffected by unusual or non-recurring items.

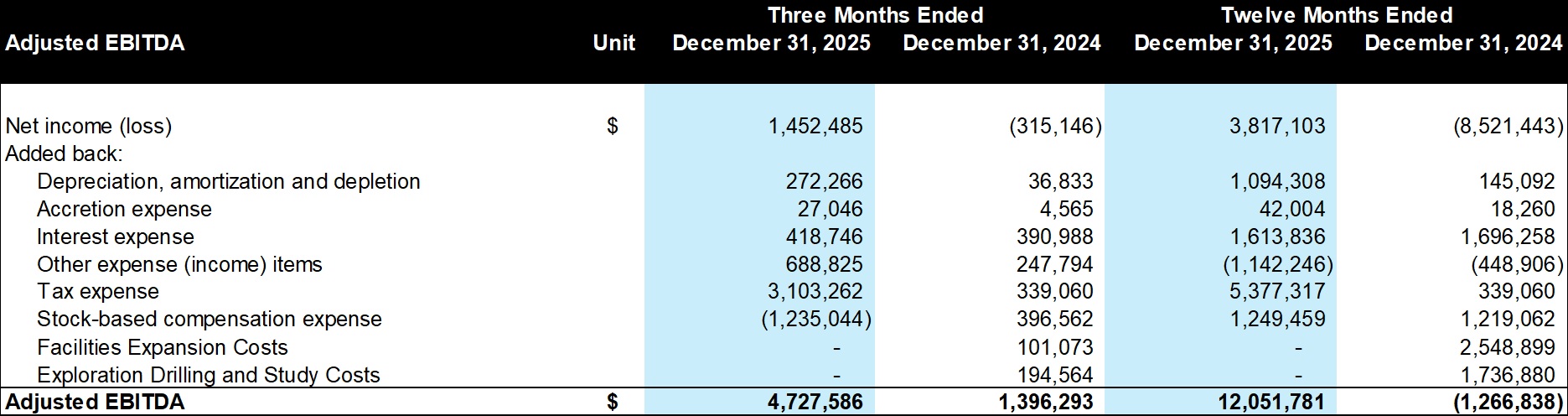

Set forth below is a reconciliation of adjusted EBITDA to net income (loss):

To view an enhanced version of this graphic, please visit:

https://images.newsfilecorp.com/files/5274/290953_tabledynaresource.jpg

We use adjusted EBITDA to evaluate our business on an ongoing basis and believe that, in addition to conventional measures prepared in accordance with GAAP, certain investors use non-GAAP measures, such as adjusted EBITDA to evaluate our performance and ability to generate cash flow. We also report this measure to provide investors and analysts with useful information about our underlying costs of operations and clarity over our ability to finance operations and capital activities separately from other activities. Accordingly, it is intended to provide additional information and should not be considered in isolation or as a substitute for measures of performance prepared in accordance with GAAP.

Adjusted EBITDA has limitations as an analytical tool. Some of these limitations include:

- adjusted EBITDA does not reflect our cash expenditures, or future requirements, for capital expenditures or contractual commitments;

- adjusted EBITDA does not reflect changes in, or cash requirements for, our working capital needs;

- adjusted EBITDA does not reflect the significant interest expense, or the cash requirements necessary to service interest or principal payments, on our debts;

- although depreciation and amortization are non-cash charges, the assets being depreciated and amortized will often have to be replaced in the future, and adjusted EBITDA does not reflect any cash requirements for such replacements;

- non-cash compensation is and will remain a key element of our overall long-term incentive compensation package, although we exclude it as an expense when evaluating our ongoing operating performance for a particular period;

- adjusted EBITDA does not reflect the impact of certain cash charges resulting from matters we consider not to be indicative of our ongoing operations; and

- Other companies in our industry may calculate their adjusted EBITDA differently than we do, limiting the usefulness as a comparative measure.

Because of these limitations, adjusted EBITDA should not be considered in isolation or as a substitute for performance measures calculated in accordance with GAAP. We compensate for these limitations by relying primarily on our GAAP results and using adjusted EBITDA only supplementally.

To view the source version of this press release, please visit https://www.newsfilecorp.com/release/290953