Gunnison Copper Announces Updated Preliminary Economic Assessment of Its Flagship Gunnison Copper Project Reporting Post-Tax NPV8 of US$2.0 Billion

Phoenix, Arizona–(Newsfile Corp. – February 25, 2026) – Gunnison Copper Corp. (TSX: GCU) (OTCQB: GCUMF) (FSE: 3XS0) (“Gunnison” or the “Company”) is pleased to announce the results of an updated NI 43-101 Preliminary Economic Assessment (“PEA” or “2026 PEA”) on its 100%-owned Gunnison Copper Project in the Cochise Mining District, Arizona, United States (“Gunnison Project”). The PEA supersedes the previous PEA on the Gunnison Project released in December 2024 (the “2024 PEA”) in all respects. All dollar amounts are in US dollars and “tons” refer to U.S. short tons (1 short ton equals approximately 0.91 metric tonnes or 2000 lbs).

Highlights:

- Conventional open pit, heap leach, SX/EW operation producing 99.999% pure copper cathode intended to supply United States energy, data center, manufacturing, and defense supply chains

- Straightforward mine plan consists primarily of oxide copper mineralized material with a life of mine material placed on the leach pad of 541 million tons at 0.43% total copper grade, including 25 million tons at 0.85% total copper grade from the Strong & Harris satellite deposit

- Primary crushing on all, and secondary crushing on some material to improve copper recoveries

- Average annual copper cathode production of 174 million pounds (“lbs”) (87 thousand tons) for the first 15 years; enough to potentially supply over 11% of the current United States domestic refined copper metal production from mineralized material1. Total copper produced 3.2 billion lbs over a 21 year mine life.

- Cash costs of $1.69, Sustaining Cash Costs of $2.00, and All-In Sustaining Cash Costs of $2.06 per pound of copper produced are in the lower half of the cost curve for copper mines globally.

- Robust project economics in a variety of copper price environments, including $4.60/lb base case:

| Copper Price Assumption: | $4.60/lb Cu Consensus | $5.75/lb Cu SPOT2 | |

| NPV8 (after-tax) | $M | 1,952 | 3,219 |

| IRR (after-tax) | % | 22.7% | 32.0% |

| Payback (after-tax) | #Years | 3.9 | 2.6 |

| Avg Annual Free Cash Flow (Y1-Y15) | $M | 366 | 514 |

- High purity limestone overburden, previously treated as waste, is now used to produce a cement co-product to alleviate the regional cement supply deficit adding $130M NPV8%

- Significant economic impact to Cochise County, State of Arizona, and the United States nationally through creation of over 53,000 jobs, $544 million in state and local county taxes, $1.37 billion in federal taxes, and $14.6 billion in total economic output3

The PEA is preliminary in nature and includes inferred mineral resources that are considered too speculative geologically to have the economic considerations applied to them that would enable them to be categorized as mineral reserves. There is no certainty that the conclusions reached in the PEA will be realized. Mineral resources that are not mineral reserves do not have demonstrated economic viability.

Dr. Stephen Twyerould, CEO, commented, “The updated PEA underscores the scale and compelling economics of the Gunnison Copper Project, positioning it as a significant future supplier to the American copper market and a key contributor to the domestic supply shortfall. At a consensus copper price of $4.60 per pound, the Project delivers an after-tax NPV8 of approximately US$2.0 billion, a 23% IRR, and an attractive 3.9 year payback, positioning Gunnison as one of the most financially compelling copper development projects in the United States. Importantly, 83% of the $692 million increase in NPV8% versus our 2024 preliminary economic assessment study is driven by operational enhancements within our control, including the addition of the high-grade Strong & Harris satellite deposit, material sorting, cement and limestone co-products, and optimization initiatives. With average annual production of 174 million pounds of 99.999% pure copper cathode in the first 15 years, lower-half-of-the-cost-curve operating metrics, and significant leverage to copper prices, we believe Gunnison offers shareholders meaningful exposure to a large-scale, long-life U.S. copper asset as we advance toward Pre-Feasibility, permitting, and project financing.”

Table 1: Key Valuation Metrics at $4.60/lb Copper Price Base Case

| Valuation Metrics (Unlevered) | Unit | 2026 PEA |

| Net Present Value @ 8% (after-tax) | $ millions | 1,952 |

| Net Present Value @ 10% (after-tax) | $ millions | 1,419 |

| Internal Rate of return (after-tax) | % | 22.7 |

| Payback Period | # years | 3.9 |

| EBITDA1 (annual average Y1-Y15) | $ millions | 488 |

| EBITDA1 (annual average Y1-Y21) | $ millions | 435 |

| Free Cash Flow1 (annual average Y1-Y15) | $ millions | 366 |

| Free Cash Flow1 (annual average Y1-Y21) | $ millions | 329 |

- Non-IFRS financial measure; see “Non-IFRS Financial Measures”.

Table 2: Key Project Metrics

| Project Metrics | Unit | 2026 PEA |

| Construction Period | # months | 24 |

| Life of Mine | # years | 21 |

| Strip Ratio | Waste : Feed | 2.56 |

| Mineralized Material Mined | million tons | 641 |

| High Purity Limestone Mined | million tons | 133 |

| Alluvium-Gravel Waste Mined | million tons | 1,007 |

| Hard-Rock Waste Mined | million tons | 501 |

| Copper Grade of Material Placed on Leach Pad | % CuT | 0.43% |

| Annual Crusher Throughput (max) | million tons | 40 |

| Copper Recovery – Global | % CuT | 68.0% |

| Oxide / Enriched Recoveries | % CuTSol | 90.2% |

| Primary Sulfide Recoveries (years 10 to 21) | % CuSu | 59.9% |

| Recovered Copper Cathode | million lbs | 3,187 |

| Average Annual Copper Production (years 1-15) | million lbs 000’s tons |

174 87 |

| Initial Capital (including contingency) | $ millions | 1,544 |

| Initial Capital Excluding Acid Plant | $ millions | 1,261 |

| Capital Intensity Excluding Acid Plant1 | $/ton Cu Capacity | 14,278 |

| Profitability Ratio | NPV8% / Initial Capex | 1.3 |

| Expansion Capital (including contingency)2 | $ millions | 682 |

| Sustaining Capital3 | $ millions | 613 |

| Cash Cost (C1)4 | $/lb Cu | 1.69 |

| Sustaining Cash Cost5 | $/lb Cu | 2.00 |

| All-In Sustaining Cash Cost6 | $/lb Cu | 2.06 |

- Capital intensity is calculated as initial capital excluding acid plant, $1,261M, divided by maximum annual copper cathode plant capacity 88.3 Ktons

- Expansion capital is expenditures to either build new facilities, for example the cement plant built in years 4-5, or to expand the capacity of initial facilities, for example increased capacity of leach pad

- Sustaining Capital are expenditures to maintain initial facilities. Includes $186 million in deferred stripping costs. Includes sustaining capital for both the copper plant and the cement plant

- Cash Cost includes mine operating, crushing and leaching, process plant operating, and general and administrative costs (“G&A”)

- Sustaining Cost includes Cash Cost, Sustaining Capex, Deferred Stripping, and Royalties

- All-In Sustaining Cost (AISC) includes Sustaining Cost, Property Taxes, Severance Taxes, and Closure Costs. It excludes expansion and initial capital, and income taxes

The PEA was completed by M3 Engineering & Technology Corporation (“M3”) of Tucson, AZ and is effective as of February 22, 2026. The Technical Report (the “Report”) summarizing the results of the PEA and prepared in accordance with National Instrument (“NI”) 43-101, will be filed on SEDAR+ and GCC’s website within 45 days of this news release.

Updated Preliminary Economic Assessment Summary

The Project is in Cochise County, Arizona, approximately 65 miles east of Tucson and is held or controlled 100% by GCC. GCC has a successful track record of permitting and community relations. This, along with the fact that the Gunnison open pit has no federal permitting nexus, on flat ground with no identified endangered or threatened species or habitat, and no historical, archaeological, or Native American artefacts identified in prior studies, indicates the Company’s prior permitting track record can be maintained.

Key Changes Versus the 2024 PEA

Key changes versus the 2024 PEA include various price deck changes beyond the control of management, such as the change in long-term copper price and various operating and capital cost escalation from 2024 to 2026, as well as non-price deck changes, including improvements such as mining the high-grade Strong & Harris satellite deposit.

Net Present Value at 8.00% discount rate is the selected metric to explain the changes since the previous PEA as this metric best captures the total economic return to the Company of the Gunnison Project.

Refer to the chart and text below for explanations of the change in valuation versus the 2024 PEA.

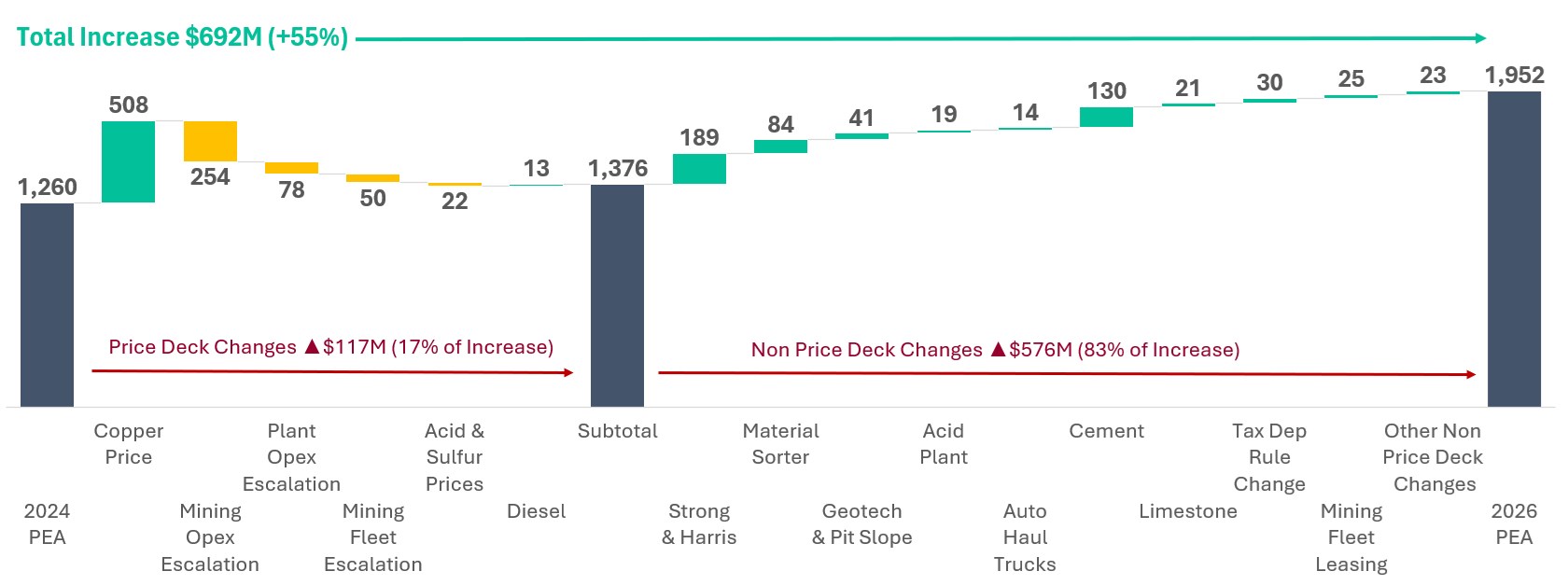

Chart 1: Change in Net Present Value 8.00% (NPV8%) – 2026 PEA versus 2024 PEA ($M)

To view an enhanced version of this graphic, please visit:

https://images.newsfilecorp.com/files/2744/285349_efb2444044252ba4_002full.jpg

Note: NPV8% variance bars should be considered approximations and include an element of estimation and interpretation. Cross correlations between variable changes may not be fully captured in each bar due to the sequence of applying changes in the financial model and other supplementary calculations performed for variables not directly changeable in the financial model.

The 2026 PEA NPV8% of $1,952M is an increase of $692M (+55%) from the 2024 PEA NPV8% of $1,260M. The increase is comprised of Price Deck changes of $117M, 17% of the increase, and Non-Price Deck changes of $576M, the remaining 83% of the increase. The following explains the key changes in more detail:

Price Deck Changes $117M – The main driver is the increase in long-term consensus copper price from $4.10/lb in the 2024 study to $4.60/lb in the 2026 study. Management uses analyst consensus given the extensive knowledge and expertise of the institutions involved and the overall reliance of the market and investors on consensus pricing. Acid, Sulfur, and Diesel prices were calculated on a delivered basis to site based on data purchased from leading industry consultants, actual delivered to site pricing, and direct discussions with logistics and commodity producers in the region. Mining opex, plant opex, and mining fleet escalation is based on inflation and other factors to escalate pricing from 2024 to 2026 real dollars and includes direct quotes from equipment manufacturers and service providers. Mining opex escalation also includes the impact of mining additional more costly blocks, due primarily to increased stripping requirements, from the bigger Gunnison main pit shell that the higher copper price makes economic to mine versus the smaller pit shell in the 2024 study.

Strong & Harris Satellite Deposit $189M – This satellite deposit, located only 1.9 miles from the processing plant, adds over 25 Mtons of high-grade material to the leach pad at 0.85% total copper grade to the processing plan over three years (Y11-Y13). Given the mining fleet and plant costs are fully supported already by the Gunnison Open Pit economics, the addition of the Strong & Harris material results in a significant NPV8% increase, extension of mine life, and increase in the leach pad head grade. No credits for zinc or silver are included in the new Strong and Harris mine and processing plan but could be considered an opportunity for later with additional processing infrastructure. As Strong & Harris is now included within the PEA, the prior technical report filed on SEDAR+ at www.sedarplus.ca entitled: “Estimated Mineral Resources and Preliminary Economic Analysis, Strong and Harris Copper-Zinc-Silver Project, Cochise County, Arizona” dated effective of September 9, 2021 has been superseded and is no longer a current technical report.

Material Sorter $84M – The mineralized Material Sorting equipment uses optical sensors to detect non-mineralized material amongst the crushed material prior to stacking on the leach pad and diverts it to waste. This reduces significantly the inclusion of non-mineralized material on the leach pad, thereby increasing the leached head grade and reducing acid consumption. In total, 97.7 Mtons of oxide material and 3.1Mtons of sulfide material is sorted to the waste stream over the life of mine, reducing mineralized material stacked and leached from 641.5 Mtons mined to 540.7 Mtons leached. The direct costs in initial capital for the equipment is $205.4M and the operating costs are $0.86/ton of mineralized material sorted and leached. Only the Martin and similar formations are included in the Material Sorting profile.

Geotechnical & Pit Slope $41M – Samples were collected in 2025 of the alluvium/conglomerate overburden at Gunnison as part of the HVA program. Their strength and geotechnical characters were analyzed and interpreted resulting in steeper pit walls than the previous study in 2024. In the alluvial overburden in 2024 the pit wall angles were determined to be 42 degrees, however the weakly cemented conglomerate component was determined to range from 45 to 49 degrees increasing in steepness with depth.

Acid Plant $19M – Due to reductions in total acid consumption in the 2026 PEA versus the 2024 PEA, the acid plant capacity was reduced by 10%, from 3,000 to 2,700 tons per day of acid production, along with other beneficial design modifications resulted in savings of $73M in initial capex. A decrease in profit per unit on third party acid sales partially offsets this improvement, due to higher operating costs.

Autonomous Haul Trucks $14M – Autonomous Haulage Systems (AHS) have become an accepted mining tool for modern mines. The effect of lowering operating costs is greater than the additional capital required for AHS. The trucks last longer, require less maintenance and are more efficient in delivering expected production rates.

Cement $130M and Limestone $21M Coproducts – In 2025, drilling and lab testing confirmed the limestone overburden on top of the Gunnison Pit to be a very high purity limestone suitable for producing several saleable products. Based on the specifications of the limestone determined by the lab testing, and market studies conducted by third party consultant firm Burgex, it was determined the highest and best use of the limestone is to process it into cement for sale into local and regional markets up to the annual amount the market is in deficit. Local market studies indicate a current deficit of over 1M tons of cement that is currently filled by foreign Mexican production with high freight costs and tariffs. As a result, a cement plant can be constructed with an output capacity of 1M tons of cement per year at an initial capital cost of $326M and it will sell cement for $157.21/ton. The plant will be constructed in Years 4 and 5 after full payback on initial capex has been reached and cumulative free cash flow is sufficient to pay for the cement plant capex. The rail facility included in the capex has a dedicated outbound capacity of 3M tons per year. Given 1M tons of cement will be sold per year, 2M tons of unrefined high grade limestone will also be sold to third parties at a price of $4.80/ton. The overall limestone overburden, at 133M tons, is a very large and special discovery and will continue to operate post Y21, the final year of copper production, until the resource is completely depleted in Y70. Opportunity exists for future expansion of the cement plant.

Tax Depreciation Rule Changes $30M – The One Big Beautiful Bill Act of 2025 permanently extended the Bonus Depreciation tax rule that permits 100% deduction of tangible property with a recovery period of 20 years or less, and other qualified improvement property, in the year of expenditure. This accelerated depreciation reduces cash income taxes paid in the earlier years of the project, improving NPV8%. The same total cash taxes are paid over the life of the mine but now are been paid later due to the accelerated deductions.

Mining Fleet Leasing $23M – The initial mining fleet is now assumed to be capital leased with interest only payments during the construction period that increases the NPV, partially offset by a 125 bps higher lease rate premium included in the lease for this feature. Mining fleet purchases included in sustaining capex are now also assumed to be leased with regular payment terms.

Other Non-Price Deck Changes $23M – All other changes

Financial Analysis

The PEA base case generates an after-tax Net Present Value of approximately $2.0 billion (at a discount rate of 8%) and an Internal Rate of Return (IRR) of 22.7%. This financial analysis is based on a non-levered cash flow model, revenues and costs priced in 2026 real US dollars, mid period discounting, and a valuation date set at the start of Project construction. The following tables detail key financial model inputs.

Table 3: Price Deck

| Price Deck Inputs | Unit | 2026 PEA |

| Copper Price | $/lb | 4.60 |

| Net Copper Premium | $/lb | 0.04 |

| Molten Sulfur Delivered – Purchases | $/ton | 160.00 |

| Sulfuric Acid Delivered – Purchases | $/ton | 210.00 |

| Sulfuric Acid Delivered – Sales | $/ton | 190.00 |

| Diesel Delivered | $/gallon | 2.96 |

| Propane Delivered | $/gallon | 2.00 |

| Cement – Sales | $/ton | 157.21 |

| Limestone – Sales | $/ton | 4.80 |

| Power – Purchases & Sales | $/kWh | 0.079 |

Price Deck Notes:

- Copper price of $4.60/lb is based on analyst consensus pricing as of February 3, 2026

- Net copper premium of $0.04/lb (metal premium $0.115/lb, or 2.5% of copper price, less freight to customer of $0.0725/lb)

- Acid buying price of $210/ton if acid is required above the acid plant’s capacity, and an acid selling price of $190/ton if excess acid is produced in any specific year. The acid selling price includes the cost of truck delivery from the Gunnison site to assumed local purchasers

- The acid plant generates electricity equivalent to a 26 MW power plant. The power generated during the life of the copper mine is completely used in the operation of the mine and process plant. Following the closure of the copper mine, power generation will be completely used by the cement plant

Table 4: Capital Expenditures

The capital cost estimates for this PEA, shown in table below, were developed with a -25% to +30% accuracy. The Company has used an overall contingency of 20% in accordance with Association of the Advancement of Cost Engineering International (AACE) Class 5 estimate guidelines.

| Capital Expenditures Inputs | Unit | Initial | Expansion | Sustaining |

| Direct Costs – Mine Costs | $ million | 294.0 | – | 77.7 |

| Direct Costs – Deferred Stripping | $ million | – | 185.7 | |

| Direct Costs – Leach Pad | $ million | 76.1 | 201.2 | – |

| Direct Costs – Crusher | $ million | 53.3 | – | – |

| Direct Costs – Ore Sorting | $ million | 205.4 | – | – |

| Direct Costs – SX-EX | $ million | 186.0 | – | – |

| Direct Costs – Freight | $ million | 52.4 | 16.0 | – |

| Direct Costs – Subtotal | $ million | 867.0 | 217.3 | 263.4 |

| Indirect Costs | $ million | 148.0 | 32.9 | – |

| Owner’s Costs | $ million | 65.6 | – | – |

| Contingency | $ million | 127.5 | 39.2 | |

| Subtotal | $ million | 1,208.1 | 289.4 | 263.4 |

| Acid Plant | $ million | 282.3 | – | – |

| Infrastructure | $ million | 53.2 | 10.8 | – |

| Sulfide Plant | $ million | – | 56.6 | – |

| Cement Plant | $ million | – | 325.5 | 349.5 |

| Total CAPEX | $ million | 1,543.7 | 682.3 | 612.9 |

Capital Expenditures Notes:

- The cement plant is built over years 4 and 5, following payback on initial capex investment. Sufficient free cash flow is generated in year 4 post-payback to fully pay for the cement plant capex

Table 5: Operating Expenditures – Copper

| Operating Expenditures – Copper Inputs | $ Millions Total | $/lb Cu Produced | $/Ton | |

| Mining – Before Deferred Stripping | 4,179 | 1.31 | $/ton mined $/ton mined $/ton mined |

1.83 |

| Mining – Limestone Credits | (231) | (0.07) | (0.10) | |

| Mining – Deferred Stripping | (186) | (0.06) | (0.08) | |

| Mining – Subtotal | 3,762 | 1.18 | $/ton mined | 1.65 |

| Processing – Heap Leach | 1,146 | 0.36 | $/ton leached | 2.12 |

| Processing – Material Sorting | 218 | 0.07 | $/ton sorted | 0.86 |

| Processing – SX/EW | 636 | 0.20 | $/ton leached | 1.18 |

| Processing – Subtotal | 2,000 | 0.63 | $/ton leached | 3.70 |

| G&A – Onsite | 142 | 0.04 | $/ton mined | 0.22 |

| G&A – Limestone Credits | (6) | (0.00) | $/ton mined | (0.01) |

| Byproduct Credits – Acid Sales | (503) | (0.16) | $/ton mined | (0.78) |

| Cash Cost (C1) | 5,396 | 1.69 | $/ton mined | 8.41 |

| Sustaining Capex – Mining | 78 | 0.02 | $/ton mined | 0.12 |

| Sustaining Capex – Deferred Stripping | 186 | 0.06 | $/ton mined | 0.29 |

| Sustaining Capex – Subtotal | 263 | 0.08 | $/ton mined | 0.41 |

| Royalties | 715 | 0.22 | $/ton mined | 1.11 |

| Sustaining Cash Cost | 6,374 | 2.00 | $/ton mined | 9.94 |

| Taxes – Property Tax | 64 | 0.02 | $/ton mined | 0.10 |

| Taxes – Severance Tax | 109 | 0.03 | $/ton mined | 0.17 |

| Taxes – Subtotal | 173 | 0.05 | $/ton mined | 0.27 |

| Closure – Reclamation (Inc. Surety Bond) | 72 | 0.02 | $/ton mined | 0.11 |

| Closure – Salvage Value | (63) | (0.02) | $/ton mined | (0.10) |

| Closure – Subtotal | 9 | 0.00 | $/ton mined | 0.01 |

| All-In Sustaining Cost (AISC) | 6,556 | 2.06 | $/ton mined | 10.22 |

- This table contains Non-IFRS financial measures; see “Non-IFRS Financial Measures”.

Operating Expenditures – Copper Notes:

- Mining operating cost estimates, prepared by Independent Mining Consultants (“IMC”), are based on an owner’s team managing mining activities, using an owner-operator model. Process operating cost estimates and G&A cost estimates were prepared by M3, as summarized in the table above (note numbers may not visually add due to rounding)

- The operating site includes numerous infrastructure and location advantages including:

- Union Pacific rail line right next to the property with a 2 km rail spur envisioned

- High voltage power lines with clean power from SSVEC

- Close to local and regional labor pools of Benson, Willcox, and Tucson

- Flat to slightly undulating land is conducive for development

- Deposit is within an enclosed hydrological basin; therefore no 404 permit is required

- No identified endangered flora or fauna on the property

- Limestone credits are the costs of mining and G&A that are attributable to the limestone/cement co-product cost and are included in the Cement operating Expenditures table below

Table 6: Operating Expenditures – Cement

| Operating Expenditures -Cement Inputs | $ Millions Total |

$/Ton Limestone Processed |

$/Ton Cement Produced |

| Mining | 231 | 2.89 | 3.53 |

| Processing – Raw Materials Processing | 612 | 7.69 | 9.38 |

| Processing – Additives | 768 | 9.64 | 11.76 |

| Processing – Energy | 1,536 | 19.28 | 23.52 |

| Processing – Labor & Staff | 718 | 9.01 | 10.99 |

| Processing – Maintenance | 811 | 10.18 | 12.42 |

| Processing – Other Costs | 693 | 8.70 | 10.61 |

| Processing – Subtotal | 5,137 | 64.49 | 78.68 |

| Freight | 845 | 10.61 | 12.95 |

| G&A – Onsite | 408 | 5.12 | 6.25 |

| G&A – Mining – Portion out of Cu | 6 | 0.07 | 0.09 |

| Byproduct Credits – Limestone – Royalty Sales | (255) | (3.20) | (3.90) |

| Cash Cost (C1) | 6,372 | 79.99 | 97.59 |

| Sustaining Capex | 350 | 4.39 | 5.35 |

| Sustaining Cash Cost | 6,722 | 84.38 | 102.95 |

| Taxes – Property Tax | 34 | 0.43 | 0.52 |

| Closure – Reclamation (Inc. Security Bonds) | 59 | 0.74 | 0.90 |

| Closure – Salvage Value | (26) | (0.33) | (0.40) |

| Closure – Subtotal | 33 | 0.41 | 0.50 |

| All-In Sustaining Cost (AISC) | 6,789 | 85.22 | 103.97 |

- This table contains Non-IFRS financial measures; see “Non-IFRS Financial Measures”.

Operating Expenditures – Cement Notes:

- Energy is the most significant operational expense for cement production, estimated at $23.52 per ton (30 percent of total operating expenses) of cement produced. This is consistent with the energy-intensive nature of the pyro processing (kiln) and grinding stages. Energy consumption is modeled using industry benchmarks of 3.5 gigajoules per ton of clinker (thermal) associated with a modern dry-process rotary kiln using a five-stage preheater, and 110 kilowatt-hours per ton of cement (electrical).

- The model estimates additive costs at $11.76 per ton (15 percent of total operating expenses). This covers the procurement and delivery of materials added to the clinker, including gypsum (to control setting time) and supplementary cementitious materials (SCMs) such as fly ash, slag or pozzolans used to produce blended cements (e.g., Type IL). It also includes potential inputs like clay or sand to adjust chemistry

- Plant-level labor and staff expenses are estimated at $10.99 per ton (13.9 percent of total operating expenses). This includes all salaries, wages, benefits and overhead for plant management, operations personnel, quality control and administrative staff at the site. While modern cement plants are highly automated, the relatively smaller scale of the Gunnison facility (1 million tons per year nameplate) results in a slightly higher labor cost per ton than the typical five percent to ten percent benchmark, reflecting diseconomies of scale in fixed labor.

Table 7: Other Financial Inputs

| Financial Inputs | Unit | 2026 PEA |

| Royalties | % | 4.50 |

| Stream Royalty Equivalent | % | 2.12 |

| State Royalty Equivalent | % | 0.50 |

| Federal Income Tax Rate | % | 21.00 |

| State Income Tax Rate | % | 4.90 |

| Net Operating Loss Opening Balance | $ millions | 106.8 |

| Bonus Depreciation | % | 100.0 |

| Working Capital Turnover – Accounts Receivable | # days | 15.0 |

| Working Capital Turnover – Accounts Payable | # days | 55.0 |

| Working Capital Turnover – Supplies | # days | 25.0 |

| Equipment Lease – Initial Fleet – Interest Rate | % | 8.48 |

| Equipment Lease – Initial Fleet – Downpayment | % | 15.0 |

| Equipment Lease – Initial Fleet – Term | # years | 7.0 |

| Closure Costs – Surety Bonds Premium | % | 1.0 |

Other Financial Inputs Notes:

- Stream deliveries apply to 3.5% of acid soluble copper from the Gunnison Pit, which comprises 80.8% of copper production, at 25% of market price which is equivalent to a 2.12% NSR royalty

- State royalty of 5.5% applies to the mineralized material mined from State land which comprises 9.1% of copper produced which is equivalent to a 0.50% NSR royalty

- Net operating loss opening balance are the accumulated tax loss carryforwards associated with the Gunnison Project and reduce future taxable income subject to an 80% limit per year

- Bonus depreciation, permanently extended by the One Big Beautiful Bill Act of 2025, permits 100% deduction of tangible property with a recovery period of 20 years or less, and qualified improvement property in the year of expenditure

- Mining fleet is assumed acquired via capital lease. The initial mining fleet assumes interest only payments during construction, a 15% downpayment, and a seven-year repayment term (i.e. 2 years interest only, penalized by a premium rate, plus 5 years of interest and principal payments)

Table 8: Profitability Metrics – Copper

| Profitability Metrics – Copper | $ Millions Total | $/Ton Processed | $/lb Cu Produced |

| Gross Revenues 1 | 14, 485 | 26.79 | 4.54 |

| Royalties | (715) | (1.32) | (0.22) |

| Net Revenue | 13,769 | 25.47 | 4.32 |

| Cash Cost (C1) – Copper | (5,396) | (9.98) | (1.69) |

| EBITDA | 8,374 | 15.49 | 2.63 |

| Depreciation | (2,814) | (5.20) | (0.88) |

| EBIT | 5,559 | 10.28 | 1.74 |

| Taxes | (1,145) | (2.12) | (0.36) |

| Closure | (9) | (0.02) | (0.00) |

| Net Earnings | 4,406 | 8.15 | 1.38 |

| Add Back Depreciation | 2,814 | 5.20 | 0.88 |

| Sustaining Capex | (263) | (0.49) | (0.08) |

| Free Cash Flow | 6,957 | 12.87 | 2.18 |

This table contains Non-IFRS financial measures; see “Non-IFRS Financial Measures”.

1 Gross Revenues includes the effects of the Triple Flag stream

Profitability Metrics – Copper Notes:

- Free cash flow of $2.18/lb of copper produced in the 2026 PEA is $0.30/lb (16%) higher than the free cash flow of $1.88/lb of copper produced in the 2024 PEA

- Metrics exclude all revenues and costs associated with the cement and limestone business

Table 9: Profitability Metrics – Cement

| Profitability Metrics – Cement | $ Millions Total |

$/Ton Limestone Processed |

$/ton Cement Produced |

| Revenues – Cement | 10,265 | 128.86 | 157.21 |

| Revenues – Limestone | 255 | 3.20 | 3.90 |

| Net Revenue | 10,520 | 132.06 | 161.11 |

| Cash Cost (C1) | (6,372) | (79.99) | (97.59) |

| EBITDA | 4,147 | 52.07 | 63.52 |

| Depreciation | (675) | (8.47) | (10.34) |

| EBIT | 3,472 | 43.59 | 53.18 |

| Taxes | (777) | (9.75) | (11.89) |

| Closure (Net of Salvage Value) | (33) | (0.41) | (0.50) |

| Net Earnings | 2,663 | 33.43 | 40.79 |

| Add Back Depreciation | 675 | 8.47 | 10.34 |

| Sustaining Capex | (350) | (4.39) | (5.35) |

| Free Cash Flow | 2,989 | 37.52 | 45.77 |

- This table contains Non-IFRS financial measures; see “Non-IFRS Financial Measures”.

Next page is Financial Model Key Inputs by Year

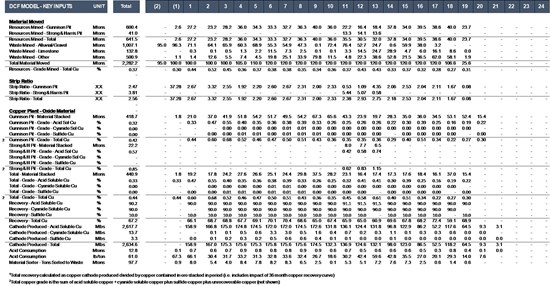

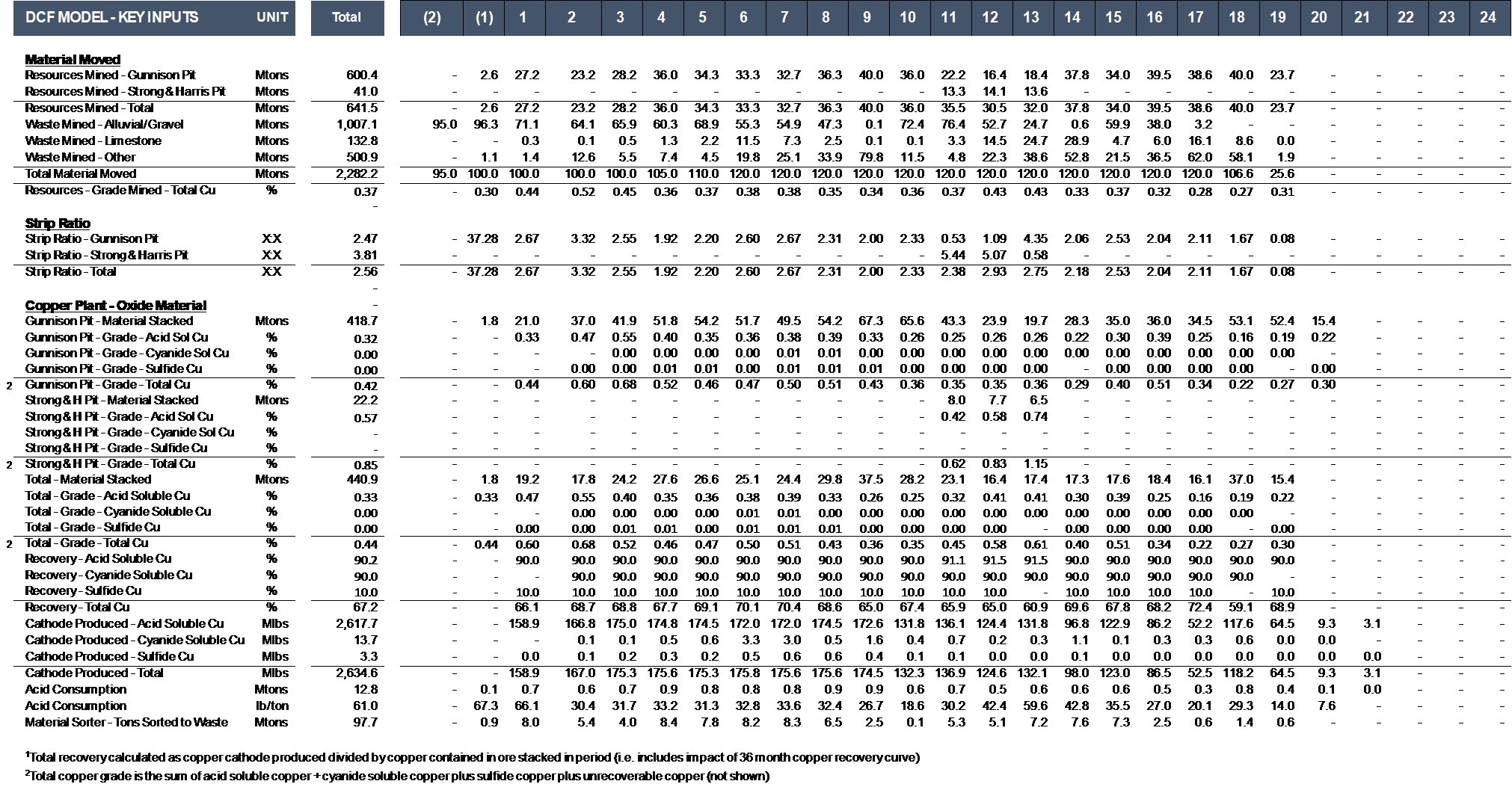

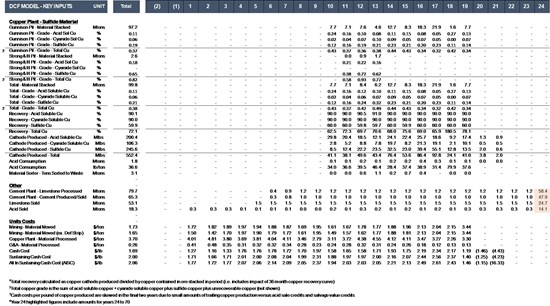

Financial Model – Key Inputs

To view an enhanced version of this graphic, please click on the image or visit:

https://images.newsfilecorp.com/files/2744/285349_efb2444044252ba4_003full.jpg

{kind=link}

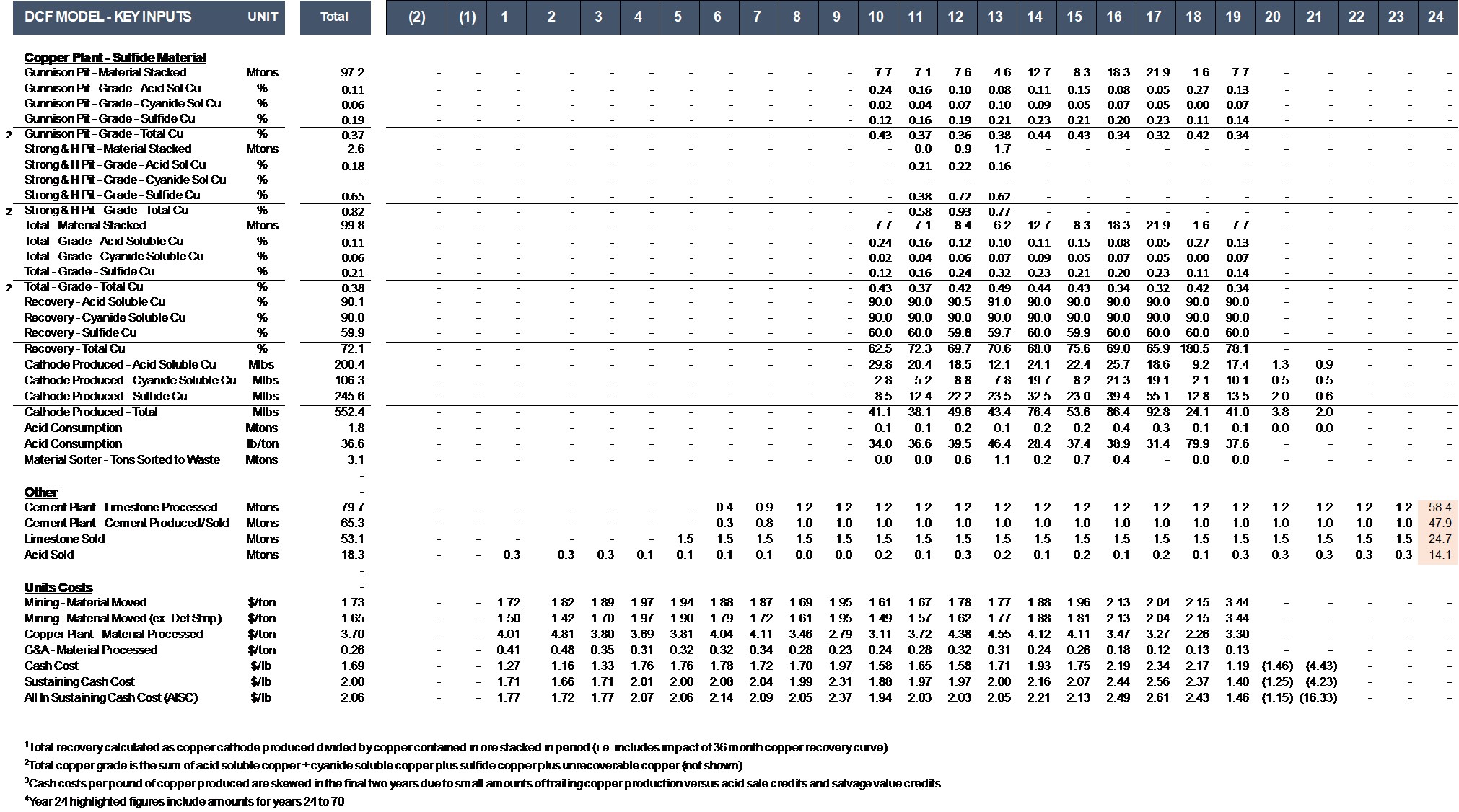

Financial Model – Key Inputs

To view an enhanced version of this graphic, please click on the image or visit:

https://images.newsfilecorp.com/files/2744/285349_efb2444044252ba4_004full.jpg

{kind=link}

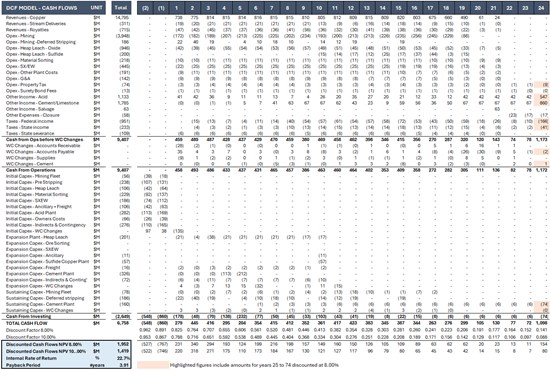

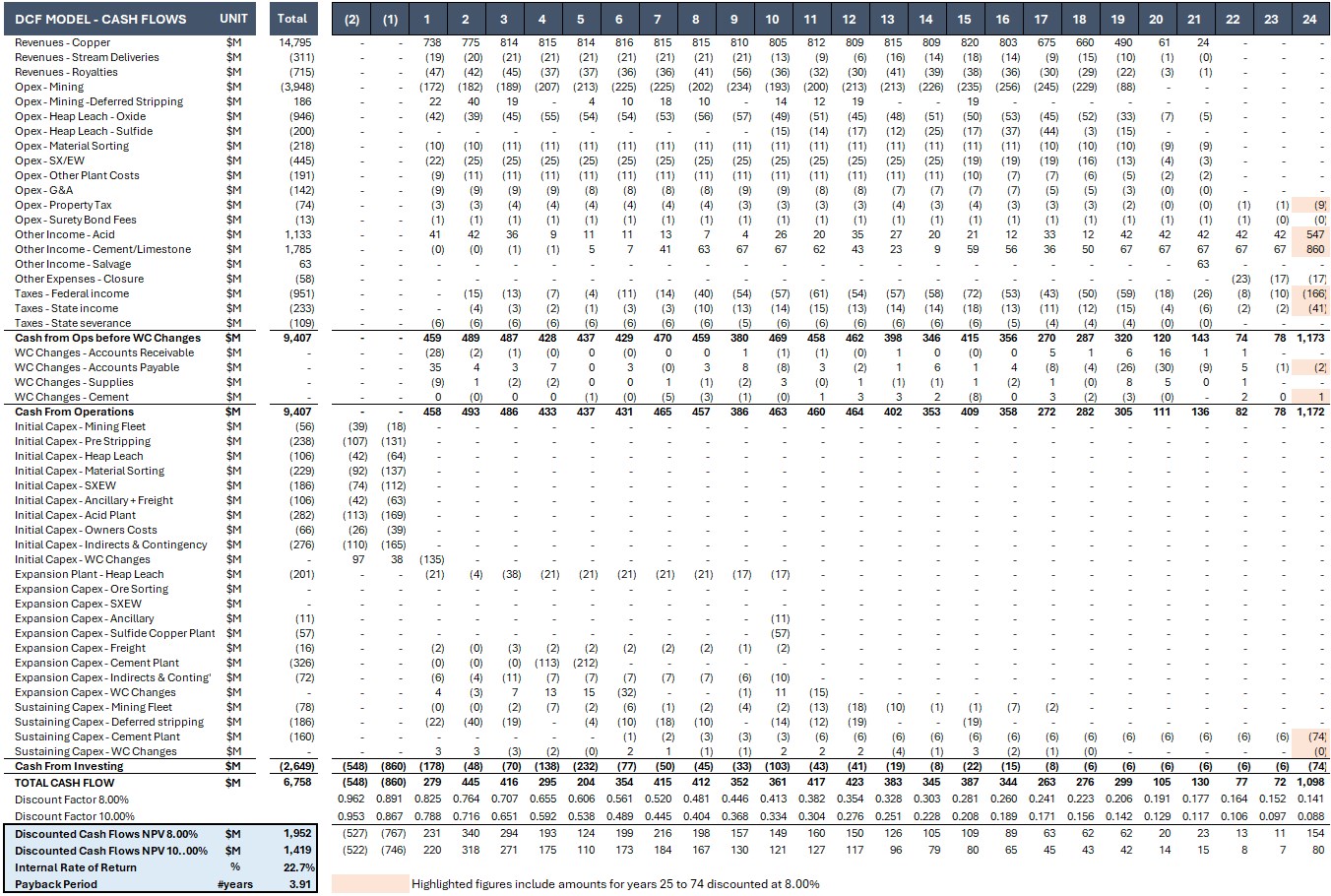

Financial Model – Cash Flows by Year

To view an enhanced version of this graphic, please click on the image and visit:

https://images.newsfilecorp.com/files/2744/285349_efb2444044252ba4_005full.jpg

{kind=link}

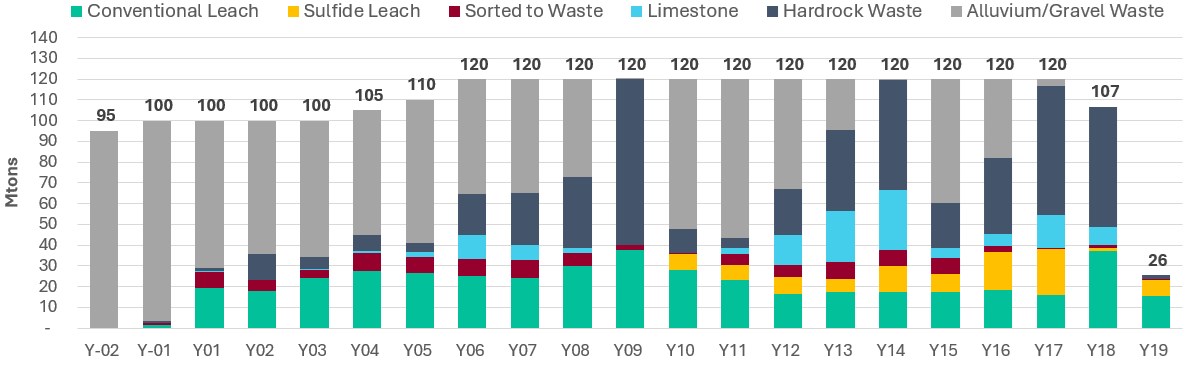

Mine Plan and Production Profile (Mtons)

To view an enhanced version of this graphic, please visit:

https://images.newsfilecorp.com/files/2744/285349_efb2444044252ba4_006full.jpg

Note: Leach numbers correspond to the tons stacking in the leach pads per year, and do not necessarily indicate copper recovery in those periods.

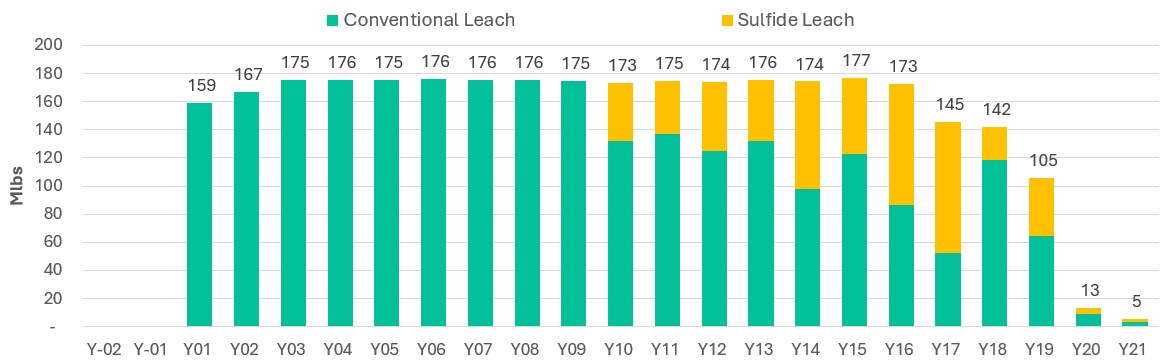

Copper Cathode Produced (Mlbs)

To view an enhanced version of this graphic, please visit:

https://images.newsfilecorp.com/files/2744/285349_efb2444044252ba4_007full.jpg

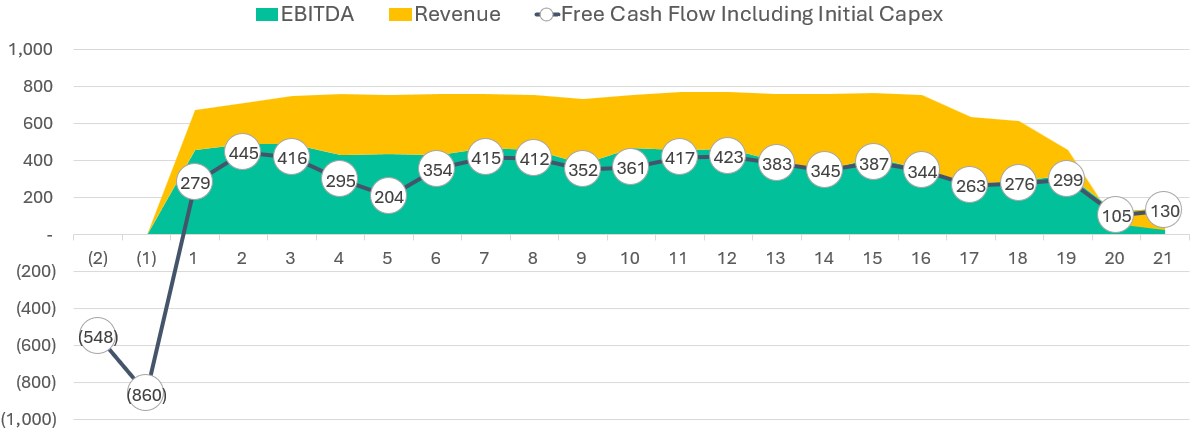

Free Cash Flow Profile ($M)

To view an enhanced version of this graphic, please visit:

https://images.newsfilecorp.com/files/2744/285349_efb2444044252ba4_008full.jpg

- This chart contains Non-IFRS financial measures; see “Non-IFRS Financial Measures”.

Years 4 and 5 free cash flows include the impact of $326M in expansion capital for the cement plant.

Mineral Resource Estimate

The mineral resource estimate for the Gunnison deposit is based on results from 122 drill holes totalling 158,785 feet and is effective as of January 23, 2026. Gunnison deposit mineral resources are classified in order of increasing geological confidence into Inferred, Indicated, and Measured categories in accordance with the “CIM Definition Standards – For Mineral Resources and Mineral Reserves” and therefore NI 43-101. GCC is not aware of any environmental, permitting, legal, title, taxation, socio-political, marketing or other issues which may materially affect its estimate of mineral resources.

The Gunnison deposit mineral resources are reported within an optimized pit at cut-offs that are reasonable given anticipated open-pit mining methods, processing costs, and economic conditions, which fulfills regulatory requirements that a mineral resource exists in such form, grade or quality and quantity that there are reasonable prospects for eventual economic extraction.

The pit-constrained mineral resources are tabulated using an internal cut-off grade of 0.05% TCu for oxide and transition, and 0.1% TCu for sulfide. No mineral resources were estimated within overburden (Tertiary/Quaternary alluvium), and the reported mineral resources are restricted to lands controlled by GCC.

| Total Resources – Gunnison Deposit | |||

| Resource Class | Short Tons (millions) |

Total Cu (%) |

Cu Pounds (millions) |

| Measured | 191.5 | 0.37 | 1,423 |

| Indicated | 654.5 | 0.31 | 3,768 |

| Measured + Indicated | 846.1 | 0.33 | 5,190 |

| Inferred | 94 | 0.21 | 397 |

- Mineral Resources that are not Mineral Reserves do not have demonstrated economic viability.

- Mineral Resources are reported within an optimized pit at a 0.05% total copper cut-off for oxide and transition material, and 0.1% cut-off for sulfide. Rounding as required by reporting guidelines, may result in apparent discrepancies between tons, grade, and contained metal content.

- The Effective Date of the Mineral Resource estimate is January 23, 2026.

The Gunnison mineral resources were modeled to reflect the detailed lithologic, structural, and oxidation modeling completed by GCC. Copper mineral domains guided by these geological controls, were interpreted on east-west vertical cross sections on 100-foot spacing, which encompass the 2.3-mile north-south and 1.3-mile east-west extents of the deposit. These domains were then used to explicitly constrain the estimation of copper grades into 50 x 100 x 25-foot (x, y, z) model blocks using 20-foot composites and inverse-distance interpolation. The grade estimation is further controlled by the incorporation of search ellipses that reflect the orientations of modeled structural zones, as well as those of favorable stratigraphic units in areas unaffected by the structures. Sequential copper assay ratios were used to define three-dimensional surfaces separating the Oxide, Transitional, and Sulfide zones of the mineralization.

All samples were prepared from manually split half-core sections on-site in Arizona. Split drill core samples were then sent to Skyline Assayers & Laboratories (“Skyline”) in Tucson, Arizona, an independent laboratory, for Total Copper (TCu) and Sequential Copper analyses, Acid Soluble Copper (ASCU) and Cyanide Soluble Cu (CNCu). Skyline is accredited with international standard ISO/IEC 17025:2005 General Requirements for the Competence of Testing and Calibration Laboratories. Analytical results for (TCu), (ASCu), and (CNCu) were reported. GCC has no relationship with Skyline Labs other than Skyline being a service provider. Standards, blanks, and duplicate assays are included at regular intervals in each sample batch submitted from the field as part of an ongoing Quality Assurance/Quality Control Program.

The mineral resource estimate for the Strong and Harris deposit is underpinned by 152 historical drillholes totaling 130,679 feet and is effective as of January 23, 2026. Strong and Harris deposit mineral resources are classified in order of increasing geological confidence into Inferred, Indicated, and Measured categories in accordance with the “CIM Definition Standards – For Mineral Resources and Mineral Reserves” and therefore NI 43-101. GCC is not aware of any environmental, permitting, legal, title, taxation, socio-political, marketing or other issues which may materially affect its estimate of mineral resources.

The pit-constrained mineral resources for Strong and Harris are tabulated using an internal cut-off grade of 0.07% TCu within optimized pit shells. No mineral resources were estimated within overburden (Tertiary/Quaternary alluvium), and the reported mineral resources are restricted to lands controlled by GCC.

| Total Resources – Strong & Harris Deposit | |||||||

| Resource Class |

Short Tons (millions) |

Total Cu (%) |

% Zn | Oz Ag/ton | Cu Pounds (millions) |

Zn Pounds (millions) |

Oz Ag (millions) |

| Inferred | 76 | 0.49 | 0.56 | 0.12 | 740 | 856 | 9 |

Notes:

- Mineral Resources that are not Mineral Reserves do not have demonstrated economic viability.

- Mineral Resources are reported within an optimized pit at a 0.07% total copper cut-off.

- Rounding as required by reporting guidelines, may result in apparent discrepancies between tons, grade, and contained metal content.

- The estimate of mineral resources may be materially affected by geology, environmental, permitting, legal, title, taxation, sociopolitical, marketing, or other relevant issues.

- The Effective Date of the Mineral Resource estimate is January 23, 2026.

The Strong and Harris mineral resources were modeled to reflect the detailed geologic and structural controls on mineralization. Copper, zinc, and silver mineral domains guided by these geological controls, were interpreted on 200-foot spacing along the approximate direction of dip (045° azimuth). While each metal was explicitly interpreted on every cross section, copper, zinc, and silver are generally spatially coincident throughout the deposit. These domains were then used to explicitly constrain the estimation of copper, zinc, and silver grades into 20 x 20 x 20-foot (x, y, z) model blocks using 10-foot composites and inverse-distance interpolation. The grade estimation is further controlled by the incorporation of search ellipses that reflect the orientations of modeled structural zones, as well as those of favorable stratigraphic units in areas unaffected by the structures. Sequential copper assay ratios were used to define three-dimensional surfaces separating the Oxide, Transitional, and Sulfide zones of the mineralization. The block model covers 3.91 square miles and extends to a maximum depth of 2,820 feet below the topographic surface.

Mr. Jeffrey Bickel, C.P.G., with the independent firm RESPEC Company LLC (“RESPEC”) of Reno, Nevada, is a Qualified Person as defined by NI 43-101 and is responsible for this mineral resource estimate. He has verified, reviewed, and approved the technical disclosure contained in this section of the news release. Mr. Bickel has verified the data underlying the results by reviewing the drilling, sampling, assay, and quality assurance and quality control data, as well as the geologic interpretations completed by GCC. Mineral resources that are not mineral reserves do not have demonstrated economic viability.

Risks

Certain risks and opportunities are associated with the Project, as is typical for mine development projects. These risks may include and are not limited to environmental permitting, title issues, taxation, public/political opposition, or legal impediments to operating this type of mining/processing operation at this location. The following Project-specific risks have been identified along with the measures that GCC envisages to mitigate the risk.

- Slope Stability. Slope recommendations received from Call & Nicholas, Inc. (“CNI”) were based on recent strength testing as well as rock quality designation (RQD) data from core holes and experience at other Arizona mines in similar rock formations. Actual slope angles may have to be decreased, increasing the amount of waste handling required.

Mitigation. Geotechnical drilling, along with further in-depth slope stability analysis, could result in achievable pit slope angles that are more shallow or steeper than the angles used in the analysis that will be presented in the report.

- Blasting Costs. Drilling and blasting in the weakly cemented alluvium overburden is assumed to be significantly more productive than in the bedrock. Overestimation of blasting productivity in the overburden would result in increased costs.

Mitigation. Additional investigation of the weakly cemented alluvium could remove uncertainties for this productivity differential.

- Mine Design Uncertainty. The tonnage expected to be placed on the leach pad could change as more drilling and engineering are completed. Metal prices, changes in metal recovery, or increases in operating costs could change the potential tonnage of heap leachable material.

Mitigation. Additional investigation as the project moves toward implementation should reduce the uncertainty.

- Copper Recovery. The heap leaching process for recovering copper from oxidized mineralization can be unpredictable. Metallurgical testing has established that coarse crushed mineralization is amenable to copper heap leaching and recovery. Metallurgical testwork results have been used to approximate results of leaching, although they may not reflect the LOM actual leach recovery performance. There is risk that additional testwork or actual performance could indicate the possibility of lower copper recoveries at the current crush size, acid application rate, or leach cycle estimates.

Mitigation. Operational strategies will involve adjusting crush sizes, flowrates and acid strengths based on operational experience to maximize infiltration rates and increase PLS grades.

- Leach Pad Flow Attenuation. Production of excess fines, compaction of lift surfaces on the leach pad, decrepitation of host rock mineralized material, and precipitation of minerals due to acid depletion could cause the formation of zones of low permeability. As with all leach pads, there is risk of poor vertical solution flow and leach pad hydrodynamics.

Mitigation. Placement and distribution of the leach material will be monitored to prevent compaction and enhance uniform distribution of leach solutions. Boreholes drilled through zones identified with low permeability can enhance vertical migration of solutions. Segregation or special treatment of materials that are identified as decrepitation (breaking down) and/or releasing fines may be necessary to mitigate this type of flow attenuation.

- Acid Consumption/Cost. The Gunnison Project relies on large volumes of sulfuric acid to liberate and dissolve copper from the leach pad materials to produce a saleable product. Acid consumption is estimated to range from 24 to 87 pounds of acid per ton of leach material based on the various rock types and carbonate content. The actual acid consumption could potentially be higher.

Mitigation. Controlling excess sulfuric acid consumption may require careful management and segregation of the materials as they are placed on the leach pad. The height of each lift could be increased to reduce the time that the lower portion is subjected to leach solutions consuming acid. Placing geomembranes or low permeability layers between lifts could isolate depleted, acid-consuming materials at the bottom of the pad. Building an acid production facility greatly reduces acid cost, which helps mitigate higher acid consumptions.Further studies into mineralized material sorting to reject high carbonate-low copper mineralization will be continued to determine the applicability and economics of this technique at a pre-feasibility study (“PFS”) level. Mineralized material sorting has the potential to reduce acid consumption in practice.

- Permitting Difficulties. Permitting for mining projects in the western US and Arizona has often been an arduous and unpredictable task in the recent past. Regulations and social attitudes can change. Although the Company has previously been able to obtain all operating permits in a reasonable time frame, there is no certainty this track record will continue.

Mitigation. Permitting difficulties for changing the mining method for the deposit can be mitigated by developing support within the local community, identifying, and fixing potential areas of contention before they arise, getting support from community leaders in advance of applying for permits. Another measure is developing realistic permitting schedules that incorporate time to deal with challenges which also helps minimize deleterious consequences.

Opportunities

Several opportunities have been identified which could enhance the viability and economic attractiveness of the Open Pit Project. Many of these opportunities may be realized by removal of risk and uncertainty that are present at the PEA level.

- Acid Consumption. Mineralized material sorting is a significant value-add opportunity for the Gunnison open pit. Greater than 80% of the mined copper is oxide mineralization, forming visually distinct blue-green and red-brown zones that are ideally suited to optical mineralized material sorting. Initial testing suggest sorting of this material has the potential to greatly reduce acid consumption and volume of material leached by removing 40 to 50 percent of the process stream as unmineralized, higher acid consuming, waste. This would result in significant savings on operating costs.

- Pit Slope Angles. The pit wall angles for the Gunnison open pit are considered reasonable based on the data available, however it is conceivable that pre-feasibility geotechnical data can steepen the pit walls in the gravel-alluvium, thus reducing pre-strip capital costs and life of mine waste mining costs.

- Copper Recoveries. The anticipated copper recovery is an estimate based on the best interpretation of existing test work. This copper recovery could be exceeded in practice. Recovery increases could improve the rate of recovery, as well as increase total copper recovered. Improvements in the rate of recovery would mean lower flows from the leach pad for the same level of copper production, lowering operational costs., Or, the increased grade could result in higher copper production (revenue) for the same operating cost. Improvements in total copper recovered have the obvious benefit of increasing total revenue during the life of the mine.

- Increased Copper Price. The current financial analysis is based on an average, long-term copper price of $4.60 per pound based on current consensus pricing. Current spot markets are currently 25% to 33% higher than long-term pricing estimates. Global demand increases for copper have the potential to drive copper prices higher, thereby increasing the economic (revenue) outlook for the Project.

- Alluvium Mining. 61% of the waste mined in the pit is weakly cemented gravel (alluvium). The current design includes reduced drill and blast costs for this gravel including free digging of the top 50 feet however it is possible even more of this material will not need any drill and blast. This will be investigated in more detail during the planned PFS.

- Alternative Mining of Alluvium. The current removal of alluvium envisions the use of blast-haul operations. There are potential cost savings by developing other means of removal such as use of conveyors, dozers, or earth movers instead of blast-load-dump equipment. These will be investigated during the PFS”.

- In-pit Leaching. In-pit leaching provides an opportunity to reduce operating costs and improve leach recovery over the life of mined mineralized material. The nature of the Gunnison deposit and aquifer would allow control of leach solutions. Permitting of in-pit leaching would be required through Arizona Department of Environmental Quality, though it is currently being employed at other properties in Arizona. Production sequencing will utilize in-pit leaching as a trade-off to the construction and maintenance of a heap leach pad during PFS work on the Gunnison open pit.

- Exploration Potential. The mining district that GCC has consolidated in recent years exhibits significant exploration potential. Modern exploration activity has not occurred in the district. District-wide data consolidation and integration should be conducted to evaluate its overall mineral potential and identify exploration targets. Exploration for the source of the porphyry copper sulfide mineralization at Gunnison has never been conclusively conducted and copper skarn deposits such as Gunnison are often associated with large nearby porphyry copper deposits. Several historic carbonate replacement deposits including the Republic and Moore deposits merit additional exploration attention. Significant areas of Earp Formation, Colina Limestone and Horquilla Limestone are under cover and have not been explored. These same formations host the mineralization in the Hermosa-Taylor deposits being developed by South 32 in southern Arizona.

- Limestone. There is potential to create additional high-value limestone products through the application of sorting technologies. This will be investigated during the PFS.

- The mine plan has not considered the potential for in-pit waste stockpiles. Some areas of the open pit may be suitable for this, reducing hauling distances and costs.

Recommendations

Based on the results of this PEA, it is recommended that GCC consider proceeding with a PFS of the open pit project which is expected to take approximately 18 months. A feasibility study will be proposed on successful completion of the PFS.

Additional drilling for resource verification and geotechnical coverage is recommended to support mine planning. Updating the acid plant design for the selected capacity is also recommended. Additional planning and costing work are required to establish the schedule and costs for the relocation of Interstate 10 and the addition of the rail spur to the Union Pacific Railroad.

Additional drilling will be required for metallurgical studies. Pilot metallurgical heap leach testing is recommended to investigate the recovery kinetics and flow characteristics for the heap leach design. In addition, mineralized material sorting studies are recommended to determine the effectiveness and economics.

A mine plan, heap leach design, SX-EW design and highway move design are necessary to complete the PFS.

GCC has proposed a list and budget for additional work that will support a Prefeasibility Study (PFS).

| Prefeasibility Study Budget for the Gunnison Project | ||||

| Detail | Gunnison | Strong & Harris | Total | |

| Resource Upgrade | $ millions | 9.3 | 6.0 | 15.3 |

| Metallurgy | $ millions | 8.2 | 3.1 | 11.3 |

| Geotechnical and Hydrology | $ millions | 0.2 | 0.8 | 1.0 |

| Pit design | $ millions | 0.4 | – | 0.4 |

| Infrastructure/PFS study | $ millions | 1.7 | – | 1.7 |

| Total | $ millions | 19.8 | 9.9 | 29.7 |

Ownership, Social License and Permitting

The Project is in Cochise County, Arizona, approximately 65 miles east of Tucson and is held or controlled 100% by GCC through its wholly owned subsidiary Excelsior Mining Arizona, Inc. (GCAZ) and Excelsior Mining Holdings Inc. (GCH).

The project is comprised of 18,796 acres including freehold land, patented land, state mineral claims and permits and BLM unpatented mining claims and excludes the Johnson Camp project. There is no federal nexus for permitting the project and all permitting is limited to State of Arizona-required permits including the Aquifer Protection Permit, Industrial Air permits and the Mined Land Reclamation Permit.

GCC has a well-developed community engagement plan that has been implemented through numerous public meetings and outreach programs. The Company intends to maintain this approach by continuing to engage with, and meet and discuss its projects with, the local and regional communities and stakeholders.

The Cochise Mining district has legacy mining assets and is a combination brownfields/greenfield site. The Company anticipates the Project will create decades of high paying jobs that will benefit the local communities and the state.

GCC has entered into an option agreement dated November 12, 2024 (the “Option Agreement”) with certain local landowners providing the option (the “Option”) for a period of six years to acquire a total of 3,906.57 acres of land (the “Option Land”). Portions of the Option Land will contain the proposed open pit and related infrastructure. The terms of the Option Agreement require an initial payment of $1,000,000, and annual payments of $250,000 in years 2, 3, 4 and 5 of the Option. The final purchase price for exercise of the Option is based on the exercise date and is set forth in the table below:

| Final Payment Date | Total Price | ||

| During the period within 1 year from Effective Date | $ | 28,000,000 | |

| During the period after 1 year but within 2 years from Effective Date | $ | 30,000,000 | |

| During the period after 2 years but within 3 years from Effective Date | $ | 31,250,000 | |

| During the period after 3 years but within 4 years from Effective Date | $ | 33,500,000 | |

| During the period after 4 years but within 5 years from Effective Date | $ | 35,750,000 | |

| During the period after 5 years but within 6 years from Effective Date | $ | 37,000,000 | |

There are certain other option agreements to acquire adjacent land holdings which will be detailed in the Report.

Royalties and Metal Stream

Greenstone Royalty: Greenstone Excelsior Holdings L.P. (“Greenstone”) holds a 3.0% gross revenue royalty over the Gunnison Project. The gross revenue royalty is defined as royalty percentage times receipts, which is the sum of physical product receipts and deemed receipts. The Greenstone royalty applies to the entirety of the Gunnison Project and production therefrom.

The Gunnison Project is also subject to a Metal Stream Agreement with Triple Flag Mining Finance Bermuda Ltd. (“Triple Flag”) that is applicable to all oxide minerals production from the parts of the Project located in the “Stream Area”. The Metal Stream Agreement is summarized in the table below, where mppa denotes million pounds per annum.

Triple Flag Metal Stream Agreement for the Gunnison Project

| Stream Deliveries | Excelsior Mining Arizona Inc. (“Seller“) is required to deliver Grade A Copper Cathodes in an amount equal to the “Payable Copper”. The amount of Payable Copper is calculated based on a percentage of the amount of copper that is sold and delivered to Offtakers under the terms of Offtake Agreements (for percentages see heading – Payable Copper). | |||||

| Payment | The Buyer pays to the Seller a price for copper equal to 25% of the daily official LME Grade A Settlement quotation for copper quoted in U.S. Dollars, as published in the Metal Bulletin. | |||||

| “Payable Copper” means a percentage of the Reference Copper equal to: | ||||||

| Payable Copper | Scenario | Stage 1 (25 mppa) |

Stage 2 (75 mppa) |

Stage 3 (125 mppa) |

||

| Upfront Deposit | 16.5% | 5.75% | 3.5% | |||

| Upfront Deposit + Expansion Option |

16.5% | 11.0% | 6.0% | |||

| At the current stage of the Project, the Buyer has made the initial Upfront Deposit ($65 million) and the Seller is ramping up to 25 mppa. | ||||||

| The “Expansion Option” provides Buyer the option to invest an additional $65 million in the event Seller approves an expansion to at least 50 mppa. | ||||||

Callinan Royalties Corporation (now a wholly owned subsidiary of Altius Minerals Corporation) holds a gross revenue royalty over the Gunnison Project. The gross revenue royalty is defined as royalty percentage times receipts which is the sum of physical product receipts and deemed receipts. The royalty rate is 1.625% while the plant capacity is less than 75 million pounds per annum and 1.5% once plant capacity is greater than or equal to 75 million pounds per annum.

Pursuant to the terms of the Bowlin option agreement, Bowlin Travel Centers, Inc. has been granted a 1% gross revenue royalty on any copper mined and processed from certain areas of the property.

The Arizona State Land Department (ASLD) owns a sliding net return royalty (2.0% to 8.0% and estimated at 5.5%), payable to ASLD and the State Trust.

The Strong & Harris property is subject to certain additional royalties that will be detailed in the Report.

Prior Operations

The Gunnison Project was previously designed as a copper in-situ recovery (“ISR”) mine using solvent extraction-electrowinning (“SX-EW”) to produce copper cathode. The ISR operation commenced ramp-up to production in 2020; however, as previously disclosed, it had operational issues related to low flow rates, so the Company began evaluating alternatives and opportunities to fix the ramp-up challenges. Well stimulation (small scale, shallow level, hydraulic fracking), has the potential to fundamentally change the performance of the wellfield and fix many of the low productivity issues. The Company has obtained a permit for well stimulation and the next step would be to conduct field trials. If well stimulation is successful, it could provide an operation with superior economics to the open pit operation and be in copper production much quicker than an open pit. However, due to the technical risks of ISR and substantially improved viability of the open pit operation, GCC intends to focus the PFS on an open pit operation as the alternative to ISR. If future financing is available for ISR activities, the Company may elect to conduct well stimulation field trials, but such field trials will not hinder the open pit studies. The Company intends to maintain the optionality of future ISR operations and well stimulation trials as this remains an asset to the Company. This includes maintaining full compliance with all regulatory and permit requirements, including maintaining hydraulic control, pumping, monitoring and regulatory reporting.

TECHNICAL REPORT AND QUALIFIED PERSONS

The Report will be filed on SEDAR+ and on GCC’s website within 45 days of the date of this news release. The Report will consist of a summary of the PEA. The Report is being prepared under the supervision of John Woodson, PE, SME-RM, of M3 Engineering & Technology Corporation, Tucson, Arizona, who is a Qualified Person that is independent of the Company. The Report will also receive contributions from the following additional Qualified Persons, who are also independent of the Company:

- Mr. John Woodson, of M3 Engineering & Technology Corporation, Tucson, Arizona (capital and operating costs, and economic analysis).

- Mr. Jeffrey Bickel of RESPEC of Reno, Nevada (geology and mineral resource).

- Mr. Jacob Richey, of IMC of Tucson, Arizona (mining methods).

- Mr. Tom Ryan, of CNI of Tucson, Arizona (pit slope angles).

- Dr. Terence P. McNulty of T.P. McNulty & Associates of Tucson, Arizona (metallurgy).

- Dr. Abyl Sydykov of M3 Engineering & Technology Corporation, Tucson, Arizona (mineral recovery).

- Mr. R. Douglas Bartlett, of Clear Creek and Associates of Phoenix, Arizona (hydrology, mining method, permitting and environment).

- Mr. Stuart Burgess, of Burgex Mining Consultants, Sandy, Utah (Limestone and cement).

Each of these Qualified Persons has reviewed and approved the technical information contained in this news release that is relevant to their area of responsibility and verified the data underlying such technical information.

ABOUT GUNNISON COPPER

Gunnison Copper Corp. is a multi-asset pure-play copper developer and producer that controls the Cochise Mining District (the district), containing 12 known deposits within an 8 km economic radius, in the Southern Arizona Copper Belt.

Its flagship asset, the Gunnison Copper Project, has a Measured and Indicated Mineral Resource containing over 846.1 million tons with a total copper grade of 0.33% (Measured Mineral Resource of 191.5 million tons at 0.37% and Indicated Mineral Resource of 654.5 million tons at 0.31%), and a preliminary economic assessment (“PEA”) yielding robust economics including an NPV8% of $2 billion, IRR of 23%, and payback period of 3.9 years. It is being developed as a conventional operation with open pit mining, heap leach, and SX/EW refinery to produce finished copper cathode on-site with direct rail link.

The PEA is preliminary in nature and includes Inferred Mineral Resources that are considered too speculative geologically to have the economic considerations applied to them that would enable them to be categorized as mineral reserves. There is no certainty that the conclusions reached in the PEA will be realized. Mineral Resources that are not Mineral Reserves do not have demonstrated economic viability.

In addition, Gunnison’s Johnson Camp Asset, which is now in production, is fully funded by Nuton LLC, a Rio Tinto Venture, with a production capacity of up to 25 million lbs of finished copper cathode annually.

Other significant deposits controlled by Gunnison in the district, with potential to be economic satellite feeder deposits for Gunnison Project infrastructure, include South Star, and eight other deposits.

For more information on Gunnison, please visit our website at www.GunnisonCopper.com.

For further information regarding this press release, please contact:

Gunnison Copper Corp.

Concord Place, Suite 300, 2999 North 44th Street, Phoenix, AZ, 85018

Melissa Mackie

T: 647.533.4536

E: info@GunnisonCopper.com

www.GunnisonCopper.com

Non-IFRS Financial Measures

This press release contains certain non-IFRS financial measures, including Capex, sustaining capital/capex, sustaining costs, EBITDA, C1 cash costs, free cash flow, and AISC. The Company believes that these measures, together with measures determined in accordance with IFRS, provide investors with an improved ability to evaluate the underlying performance or expected performance of the Company. Non-IFRS measures do not have any standardized meaning prescribed under IFRS, and therefore they may not be comparable to similar measures employed by other companies. The data is intended to provide additional information and should not be considered in isolation or as a substitute for measures of performance prepared in accordance with IFRS.

Non-IFRS financial measures used in this press release and common to the copper mining industry are defined below.

C1 Cash Cost and Total Cash Operating Cost: C1 cash cost and Total Cash Operating Cost are reflective of the cash cost incurred at each processing stage, from mining through to recoverable copper delivered to the market, net of any by-product credits, including mine operating, process plant operating, and general and administrative costs.

All-in Sustaining Costs (“AISC”): AISC is reflective of all of the expenditures that are required to produce a pound of copper from operations. AISC reported in the PFS includes total cash costs, sustaining capital, expansion capital and closure costs, but excludes corporate general and administrative costs and salvage.

Free Cash Flow or FCF: Free cash flow is net cash flow provided from operating activities less sustaining capital expenditures.

Capital expenditures are classified as either sustaining capital expenditures or expansion capital expenditures, depending on the nature of the expenditure. Sustaining capital expenditures typically represent capital expenditures including ongoing replacement of mine equipment and other capital facilities and other capital expenditures and is calculated as total additions to property, plant and equipment (as reported on the interim condensed consolidated statements of cash flows), less expansion capital expenditures. Expansion capital expenditures represent capital expenditures for major projects, such as new facilities (e.g. cement plant) or to increase initial capacities.

CAUTIONARY NOTE REGARDING FORWARD-LOOKING STATEMENTS:

Certain statements contained in this release constitute forward-looking information within the meaning of applicable Canadian securities laws. Such forward-looking statements relate to the intention to deploy the Nuton® technology at the Johnson Camp mine and future production therefrom; the continued funding of the stage 2 work program by Nuton; the details and expected results of the stage two work program; future production and production capacity from the Company’s mineral projects; the results of the 2026 PEA on the Gunnison Project; planned budgets and timelines for future development of the Gunnison Project; and the exploration and development of the Company’s mineral projects.

In certain cases, forward-looking information can be identified by the use of words such as “plans”, “expects” or “does not expect”, “budget”, “scheduled”, “estimates”, “forecasts”, “intends”, “anticipates” or “does not anticipate”, or “believes”, or variations of such words and phrases or state that certain actions, events or results “may”, “could”, “would”, “might”, “occur” or “be achieved” suggesting future outcomes, or other expectations, beliefs, plans, objectives, assumptions, intentions or statements about future events or performance. Forward-looking information contained in this news release is based on certain factors and assumptions regarding, among other things, Nuton will continue to fund the stage 2 work program, the availability of financing to continue as a going concern and implement the Company’s operational plans, expectations regarding the receipt of 48C tax credits, the estimation of mineral resources, the realization of resource and reserve estimates, copper and other metal prices, the timing and amount of future development expenditures, the estimation of initial and sustaining capital requirements, the estimation of labour and operating costs (including the price of acid), the availability of labour, material and acid supply, receipt of and compliance with necessary regulatory approvals and permits, the estimation of insurance coverage, and assumptions with respect to currency fluctuations, environmental risks, title disputes or claims, and other similar matters. While the Company considers these assumptions to be reasonable based on information currently available to it, they may prove to be incorrect.

Forward-looking information involves known and unknown risks, uncertainties and other factors which may cause the actual results, performance or achievements of the Company to be materially different from any future results, performance or achievements expressed or implied by the forward-looking information. Such factors include risks related to the Company not obtaining adequate financing to continue operations, the Company receives less 48C tax credits than expected, Nuton failing to continue to fund the stage 2 work program, the breach of debt covenants, risks inherent in the construction and operation of mineral deposits, including risks relating to changes in project parameters as plans continue to be redefined including the possibility that mining operations may not be sustained at the Gunnison Copper Project, risks related to the delay in approval of work plans, variations in mineral resources and reserves, grade or recovery rates, risks relating to the ability to access infrastructure, risks relating to changes in copper and other commodity prices and the worldwide demand for and supply of copper and related products, risks related to increased competition in the market for copper and related products, risks related to current global financial conditions, risks related to current global financial conditions on the Company’s business, uncertainties inherent in the estimation of mineral resources, access and supply risks, risks related to the ability to access acid supply on commercially reasonable terms, reliance on key personnel, operational risks inherent in the conduct of mining activities, including the risk of accidents, labour disputes, increases in capital and operating costs and the risk of delays or increased costs that might be encountered during the construction or mining process, regulatory risks including the risk that permits may not be obtained in a timely fashion or at all, financing, capitalization and liquidity risks, risks related to disputes concerning property titles and interests, environmental risks and the additional risks identified in the “Risk Factors” section of the Company’s reports and filings with applicable Canadian securities regulators.

Although the Company has attempted to identify important factors that could cause actual actions, events or results to differ materially from those described in forward-looking information, there may be other factors that cause actions, events or results not to be as anticipated, estimated or intended. Accordingly, readers should not place undue reliance on forward-looking information. The forward-looking information is made as of the date of this news release. Except as required by applicable securities laws, the Company does not undertake any obligation to publicly update or revise any forward-looking information.

1 Based on USGS reported 2025 primary refined copper production of 790Ktons; 2 COMEX spot price at Feb 22, 2026

3 Independent Economic Impact Study conducted by the Eller Partnerships Office at the University of Arizona Oct’25

![]()

To view the source version of this press release, please visit https://www.newsfilecorp.com/release/285349