Shell plans to invest $20 billion in the Bonga South West deepwater project offshore Nigeria, citing improved political stability, policy consistency, and leadership as key factors driving its confidence in the country’s energy sector.

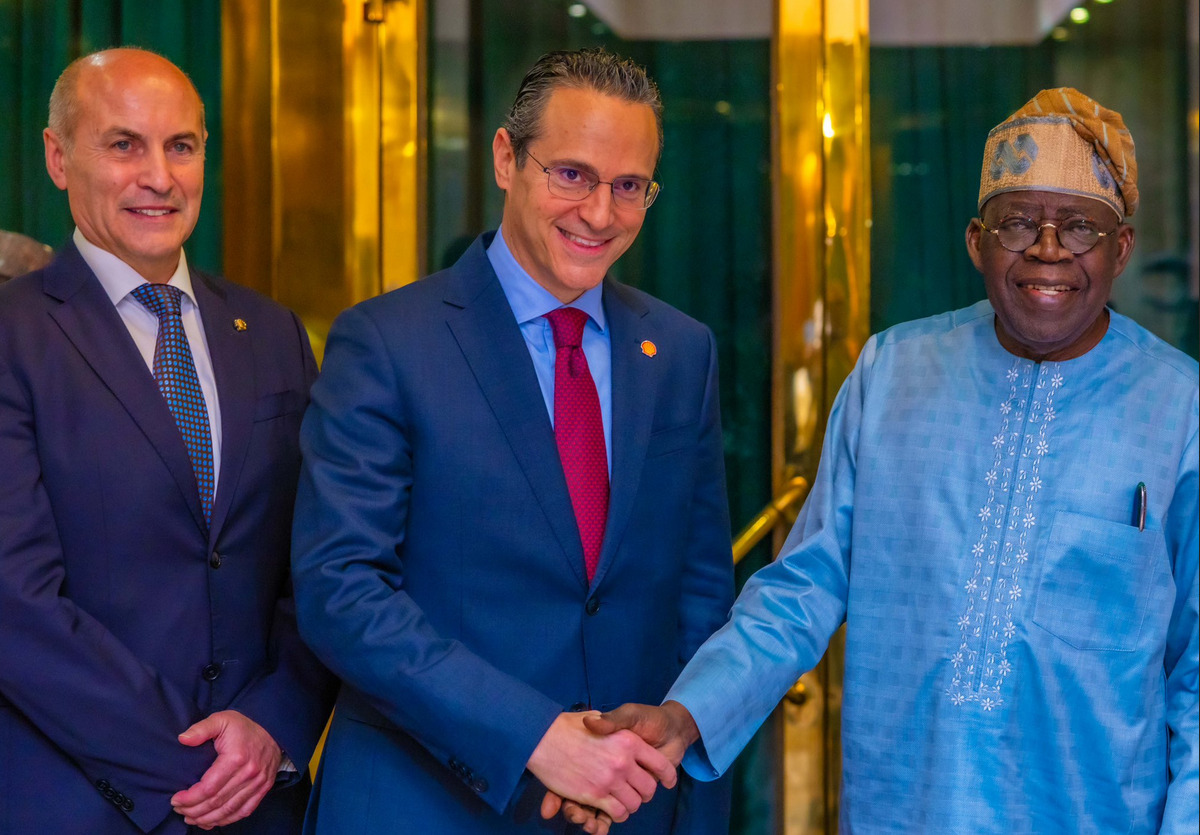

The Chief Executive Officer of Shell Plc, Wael Sawan, disclosed the company’s investment plans during a meeting with President Bola Tinubu in Abuja.

Sawan said that Nigeria now stands out as one of the most attractive destinations for capital allocation within Shell’s global portfolio.

“We think there is more to invest here, and we understand the vision that you (President Bola Tinubu) have for the country, and so we are indeed working on a project, Bonga Southwest, that could potentially, if we get to an FID stage, see us, with the partners, invest around $20 billion in foreign direct investment,” Mr Sawan said.

Shell CEO explained further that half of the $20 billion will be capital, and the other half will be the operating expenses and the likes that will come into the country.

Mr Sawan praised Nigeria’s human capital, describing Nigerian professionals within Shell’s global operations as one of the company’s largest expatriate talent pools, many of whom, he said, are expected to return home to contribute to national development.

The proposed investments underscore a gradual return of confidence by international oil companies (IOCs) in Nigeria, Africa’s largest oil producer, after years of declining capital inflows driven by regulatory uncertainty, security challenges and project delays.

Meanwhile, Chief Executive Officer of NNPC Limited, Bayo Ojulari, said the Tinubu administration’s reform agenda has helped unlock long-standing bottlenecks in the oil and gas sector, paving the way for major investment decisions and stalled project approvals.

Ojulari noted that improvements in policy clarity, fiscal terms and regulatory processes have created a more predictable operating environment for investors, particularly in capital-intensive deep offshore projects.

“Reforms implemented by the current administration have addressed several structural constraints that previously hindered investment flows into the sector,” he said. “This has enabled critical milestones, including asset divestments, project approvals and renewed engagement by international partners.”

According to Ojulari, Shell has already taken a Final Investment Decision (FID) of $5 billion on the Bonga North project, a deep offshore development expected to add significant production capacity once completed. In addition, the company has approved a further $2 billion for gas-related developments, reinforcing Nigeria’s strategic focus on natural gas as a transition fuel.

Deep offshore assets account for a significant share of Nigeria’s oil production and export earnings, making them critical to foreign exchange inflows and fiscal stability. Analysts note that renewed IOC activity in this segment could help reverse production declines and strengthen government revenues amid persistent macroeconomic pressures.

The Tinubu administration has repeatedly stated that its reforms in the oil and gas industry are designed to restore investor confidence, boost crude oil and gas production, and position Nigeria as a competitive destination for global energy capital. Key measures have included streamlining regulatory approvals, improving fiscal terms, and strengthening the governance framework under the Petroleum Industry Act.

If fully realised, Shell’s proposed $20 billion investment could significantly strengthen Nigeria’s upstream capacity, accelerate gas development and reinforce the country’s role in global energy supply chains. The investments are also expected to create jobs, deepen local content participation and support technology transfer across the oil and gas value chain.

Shell’s renewed commitment may mark a turning point in the Nigerian oil and gas industry.